The Big Picture

Australian markets closed the week in positive territory, with attention focused on shifting geopolitical developments, oil price volatility and continued pressure on mega‑cap technology stocks. Equities initially rallied on optimism that the conflict in the Middle East could de‑escalate, however sentiment later weakened as conflicting headlines undermined confidence in a near‑term resolution. Over the weekend, the Iranian‑backed Houthis in Yemen entered the conflict, firing ballistic missiles into Israel for the first time since the war began.

In Australia, Treasurer Jim Chalmers and Employment Minister Amanda Rishworth have called for an above‑inflation rise in the minimum wage as part of the Fair Work Commission’s annual review, with around 2.7 million Australians on the minimum wage ($948 per week) or award wage. Chalmers has also warned that inflation could rise as high as 5% once the impact of the Middle East conflict flows through, noting that headline inflation eased to 3.7% in February before the war’s effects. Fuel shortages escalated during the week, prompting Prime Minister Anthony Albanese to call another emergency national cabinet meeting, with disruptions reported across freight and waste services. The government says that 600 service stations have run out of at least one type of fuel. Internationally, the Philippines declared a state of emergency and European jet fuel imports are expected to fall by 40% this week, with airlines warning of potential shortages within weeks. In response to the conflict, Qantas has cut Jetstar flights to New Zealand.

The Organisation for Economic Co-operation and Development (OECD) lowered its European growth outlook for 2026, citing the Middle East conflict and its impact on costs and demand. The OECD now forecasts eurozone growth of 0.8%, down from 1.2%, and has cut its UK growth forecast from 1.2% to 0.7%.

In the week ahead, markets will watch for signs of de‑escalation in the Middle East and the eurozone’s first inflation print since the start of the war. In Australia, the RBA’s meeting minutes will be released.

2026 Euroz Hartleys Investor Conference Recap

Senior Investment Dealer Cooper Rogers recently attended the 26th instalment of the Euroz Hartleys conference, which was the largest to date, with approximately 130 investors and around 80 presenting companies. The attendee mix was high-quality, with strong representation from leading Western Australian industrials and key resource sectors.

The conference coincided with heightened global macroeconomic volatility, with discussions dominated by fuel supply concerns and the ongoing Iran conflict, which is showing no signs of easing. This drove a clear investor focus on cost resilience and earnings defensiveness.

In the resources sector, the recent pullback in gold prices is beginning to highlight what investors perceive as attractive entry points. Conversations shifted toward valuation support, capital discipline and near-term catalysts rather than momentum. Ora Banda Mining (ASX: OBM), Minerals 260 (ASX: MI6), Emerald Resources (ASX: EMR), Forrestania Resources (ASX: FRS) and Genesis Minerals (ASX: GMD) were among the standout names.

Within the industrials sector, there was a clear rotation toward companies perceived to be insulated from rising cost pressures. While the resource-linked industrials companies have performed strongly over the past six months, investor focus is now shifting toward underlying demand drivers and earnings durability. The most favoured thematics with tailwinds were energy and electrification, data centre infrastructure, defence and property. Southern Cross Electrical Engineering (ASX: SXE), Austal (ASX: ASB), Duratec (ASX: DUR), Cedar Woods Properties (ASX: CWP), Civmec (ASX: CVL) and GenusPlus Group (ASX: GNP) stood out as preferred exposures, reflecting a combination of resilience, thematic alignment and visible growth pipelines.

Stock Watch

Tuas (ASX: TUA), mobile and broadband telecommunication services provider, reported its first half 2026 result. The result beat expectations on all fronts, reflecting the continued strength of its Simba‑branded operations in Singapore. We believe Tuas is well positioned to continue its growth trajectory over the medium term. This will be driven by continued market share gains in mobile and fibre broadband subscribers, which have accelerated over the last six months. The next catalyst for growth is the approval of Tuas’ acquisition of M1 Limited, Singapore’s third largest telco, and its integration to harness the scale of a much larger operation.

The Snowtown Wind Farm II is a 270-megawatt wind farm located on the Barunga and Hummocks Ranges in South Australia, generating, on average, enough energy for 175,000 households per year. The energy generated by the wind farm is contracted to Origin Energy (ASX: ORG) through a long-term offtake agreement running to 2035, providing stable cash flows, protection against inflation and returns largely uncorrelated to public markets. WAM Alternative Assets (ASX: WMA) invests in the Snowtown Wind Farm II through its investment partner Palisade Investment Partners, alongside several Australian super funds and institutional investors.

In the Media

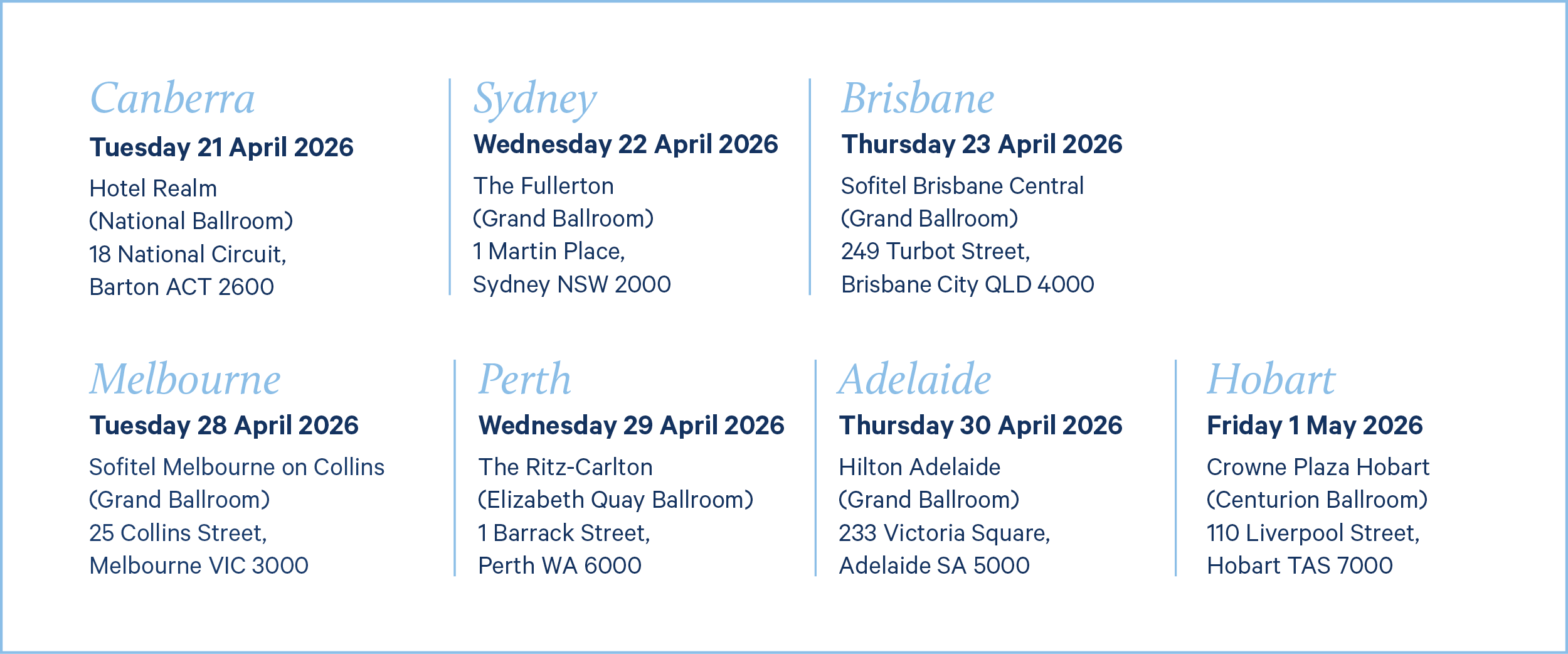

2026 National Shareholder Presentations

The Wilson Asset Management and Future Generation teams look forward to connecting with shareholders across Australia at the 2026 National Shareholder Presentations. Register here and see below for the event dates

You asked, we answered

How does WAM Global (ASX: WGB) pay fully franked dividends if it invests in global companies?

WAM Global is an Australian company that invests in other companies that are listed on global exchanges. When WAM Global realises a profit, we pay tax in Australia. It is that tax that generates the franking credits, allowing us to pay fully franked dividends to our shareholders. Across our other listed investment companies (LICs) such as WAM Leaders (ASX: WLE) and WAM Microcap (ASX: WMI), our ability to consistently pay fully franked dividends, comes from two sources. First, we pay tax on realised profits. Second, we receive franked dividends from the Australian companies that we invest in, from which we can pass through franking credits received to our shareholders. Historically, the majority of franking credits generated comes from the tax we pay on realised profits.

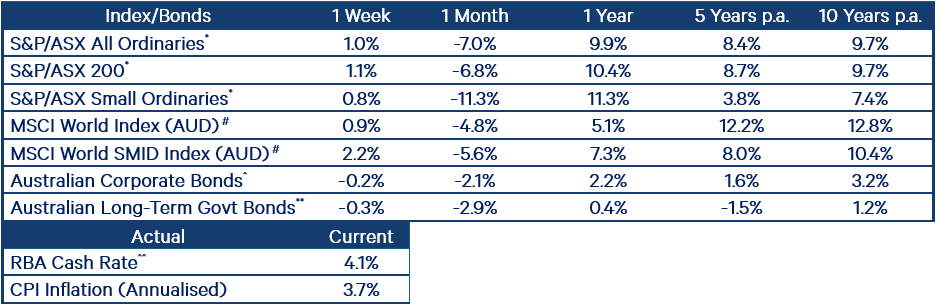

Index return performance table