The big picture

Australian equities increased over the week, with a strong mid-week rebound giving way to a weaker finish on Friday against a backdrop of renewed tension in the Middle East. While commentary from Australian banks during reporting season and the broader conference circuit suggested corporate Australia remains resilient, conditions are becoming more uneven. Strength is still evident in commodity-linked parts of the market, while consumer facing businesses are seeing more cautious spending behaviour and persistent input cost pressure.

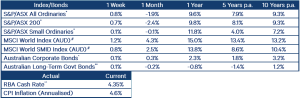

The Reserve Bank of Australia (RBA) increased the cash rate by 0.25% (25 basis points) to 4.35%, its third increase this year. Australian interest rates appear to be nearing their peak, with policy makers signalling a likely pause as they balance economic growth against elevated inflation.

Globally, equities found support from an improving US economic backdrop, with the technology sector outperforming on continued enthusiasm around artificial intelligence (AI). Of the 440 S&P 500 companies that have reported first-quarter results, 83% beat consensus earnings estimates compared with a long-term average of 67%. However, consumer sentiment has fallen to a record low as higher petrol prices and tariff concerns weigh on confidence.

Looking ahead, the Australian Federal Budget will be released tomorrow, Tuesday 12 May, and is expected to include proposed changes to capital gains tax (CGT), negative gearing and trusts. For financial markets, the key question will be whether any change to the tax treatment of productive assets begins to alter investor behaviour and capital allocation. Investors will also be watching the Westpac Consumer Confidence Index for May, data on home loans, the Wage Price Index and consumer inflation expectations.

Offshore, geopolitics is likely to remain the swing factor, alongside economic data releases from the US including the Consumer Price Index (CPI) and the Producer Price Index (PPI), retail sales and industrial production, as investors test whether inflation is re-accelerating.

In the media: Opposition to the proposed changes to capital gains tax

Chairman and Chief Investment Officer Geoff Wilson AO published an op-ed in today’s Australian Financial Review regarding the Government’s proposed changes to capital gains tax ahead of tomorrow’s May Budget, which you can read here. The proposal to abolish the 50% capital gains tax discount and return to inflation indexation would fundamentally change how Australians save, invest and build long-term wealth. It is a tax on aspiration.

The Government has framed this as a housing measure and a matter of ‘intergenerational fairness’. In reality, the proposed changes extend far beyond property into shares, small businesses, family farms and other long-term investments Australians rely on to build businesses and financial security, and fund their retirement.

At Wilson Asset Management, we believe all Australians should be treated fairly when investing in the share market. We will continue advocating for policies that encourage long-term investment, productivity and aspiration across the Australian economy.

Macro in a minute: RBA interest rate decision review and 2026/27 Budget preview

Portfolio Strategist Damien Boey shared insights on the RBA’s recent monetary policy shift, unpacking the implications of the latest rate hike to 4.35% and Governor Bullock’s more nuanced outlook for future interest rate settings. He highlights how inflation pressures, petrol prices and geopolitical uncertainty are shaping the economic backdrop, while also providing the RBA with flexibility as new data emerges. Damien also discussed the potential impact of fiscal restraint and bond market dynamics, noting that opportunities may emerge in rate-sensitive areas such as growth stocks, real estate investment trusts and consumer discretionary sectors as rates begin to ease, particularly heading into 2027. Watch Damien’s insights here.

Stock watch

HMC Capital (ASX: HMC), a diversified alternative asset manager with exposure to digital infrastructure, private credit and real estate, presented at the annual Macquarie Equities Conference this week. The investment team attended the conference, where management reaffirmed FY26 guidance and announced the divestment of the Chicago (CHI1) data centre facility. The company’s balance sheet continues to support accretive inorganic and organic growth opportunities. Combined with exposure to attractive long‑term structural themes such as digital infrastructure, private credit and real estate, the latest update reinforces the investment team’s view that the company is well positioned to deliver attractive long‑term earnings growth.

Portfolios held in: WAM Capital (ASX: WAM), WAM Research (ASX: WAX) and Wilson Asset Management Founders Fund

WAM Alternative Assets’ (ASX: WMA) real estate partner, Wentworth Capital, acquired a high-quality life sciences campus in North Ryde, Sydney in 2025, occupied by government and research tenants. The asset has approximately 12,000 square metres (sqm) of purpose-built laboratory, including a CSIRO research facility, along with around 40,000 sqm of surplus land that provides opportunities for future development.

The investment offers a combination of defensive, long-duration income from predominantly government and institutional tenants, alongside attractive value-add and development potential over time. Exposure to the life sciences sector is particularly compelling given structural demand tailwinds, including increasing healthcare expenditure, world class domestic research institutions and ongoing government support for research and innovation. This investment demonstrates how partnering with specialist managers like Wentworth Capital can provide access to high-quality real assets in undersupplied segments of the market.

Portfolios held in: WAM Alternative Assets (ASX: WMA)

You asked, we answered

Q. I heard Geoff’s comment on CGT and a discussion paper you have written. Where can I access that?

A. Our discussion paper will be made available via our website later this week. If you would like us to send it directly to you please let us know by replying to this email directly or by emailing us at [email protected].

In focus

Market imbalances can create some of the most attractive long-term investment opportunities. In our view, the current environment in opportunistic real estate is a clear example of this1. Australia continues to punch above its weight as a destination for global real estate capital, ranking as the sixth largest commercial real estate investment market and the fourth largest destination for cross-border investment, despite accounting for only around 2% of global GDP. Following several years of rising interest rates, unlisted property valuations have declined and remained subdued, even as listed real estate markets rebounded strongly in 2025. This divergence between listed and unlisted real estate performance has historically created attractive entry points for long-term investors.

As Nick Kelly, Portfolio Manager for WAM Alternative Assets notes:

|

“We’re seeing a rare window where high-quality real estate assets are available at valuations that don’t reflect their long-term fundamentals. This creates attractive opportunities for investors who are looking beyond short-term market volatility.” |

Wilson Asset Management provides investors with access to these opportunities through opportunistic real estate exposures within WAM Alternative Assets. One example is our partnership with Wentworth Capital, a specialist real estate manager focused on acquiring institutional-quality assets that are undervalued or operationally under-optimised.

Index returns performance table