Latest market news

How Woolworths can turn it around in the face of regulatory scrutiny, political pressure to reduce food prices

ANZ taps Oliver Wyman for deep dive into culture and governance within insto bank, markets unit

ASX earnings outlook trimmed on rising costs for industrials and revenue weakness for resources

30 June 2026

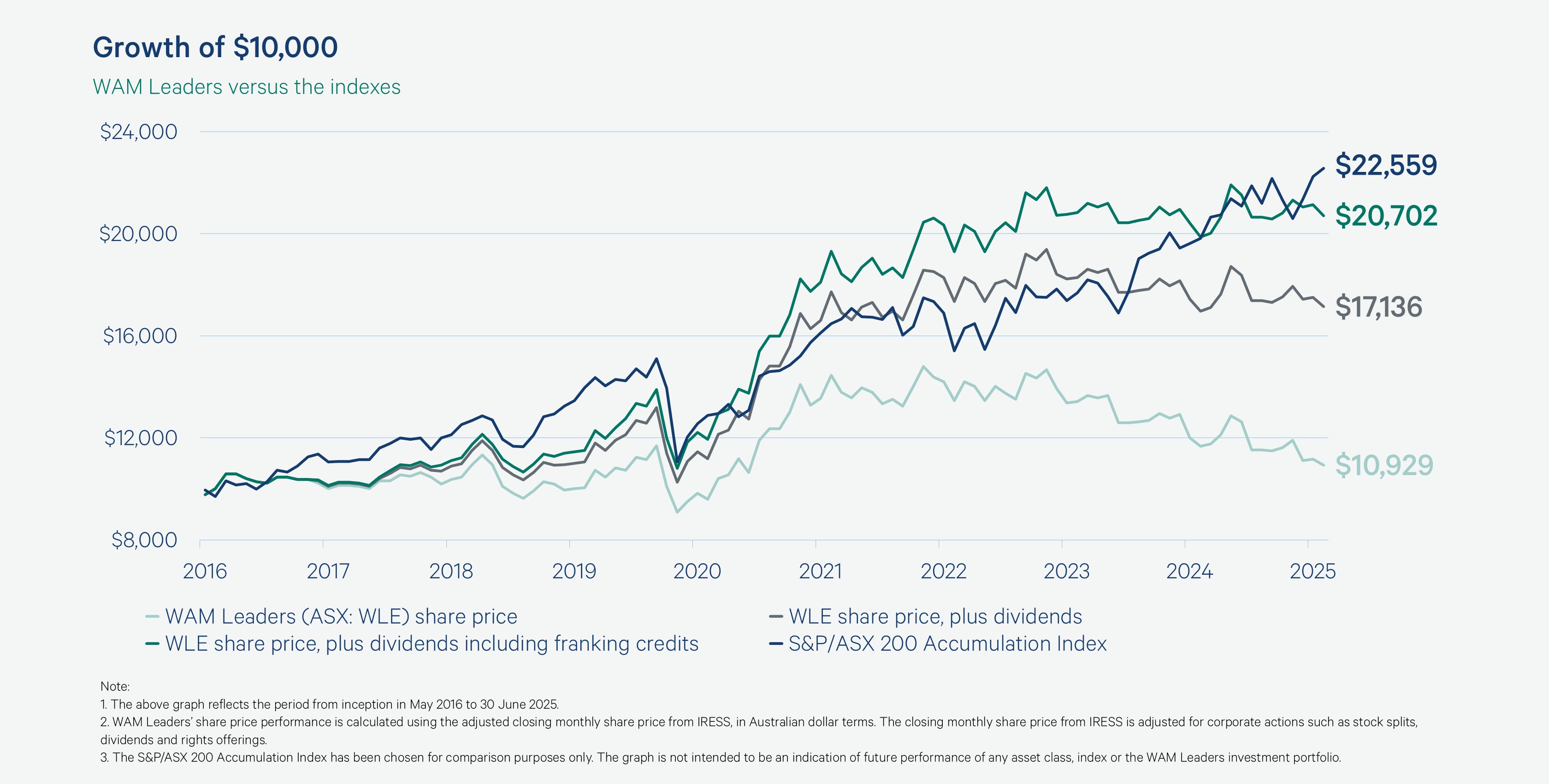

Listed: May 2016

WAM Leaders provides investors with exposure to an active investment process focused on identifying large-cap companies with compelling fundamentals, a robust macroeconomic thematic and a catalyst. The Company’s investment objectives are to deliver a stream of fully franked dividends, provide capital growth over the medium-to-long term and preserve capital.

NTA before tax

$1.33

Annualised fully franked interim dividend

9.6cps

Annualised fully franked interim dividend yield

7.2%

Grossed-up dividend yield

10.3%

Dividends paid since inception

67.55cps

Dividends paid since inception, when including the value of franking credits

96.5cps

Assets

$1.8bn

Investment portfolio performance (% p.a. since May 2016)

12.0%

Investment portfolio performance is before expenses, fees, taxes and the impact of capital management initiatives to compare to the relevant index which is before expenses, fees and taxes.

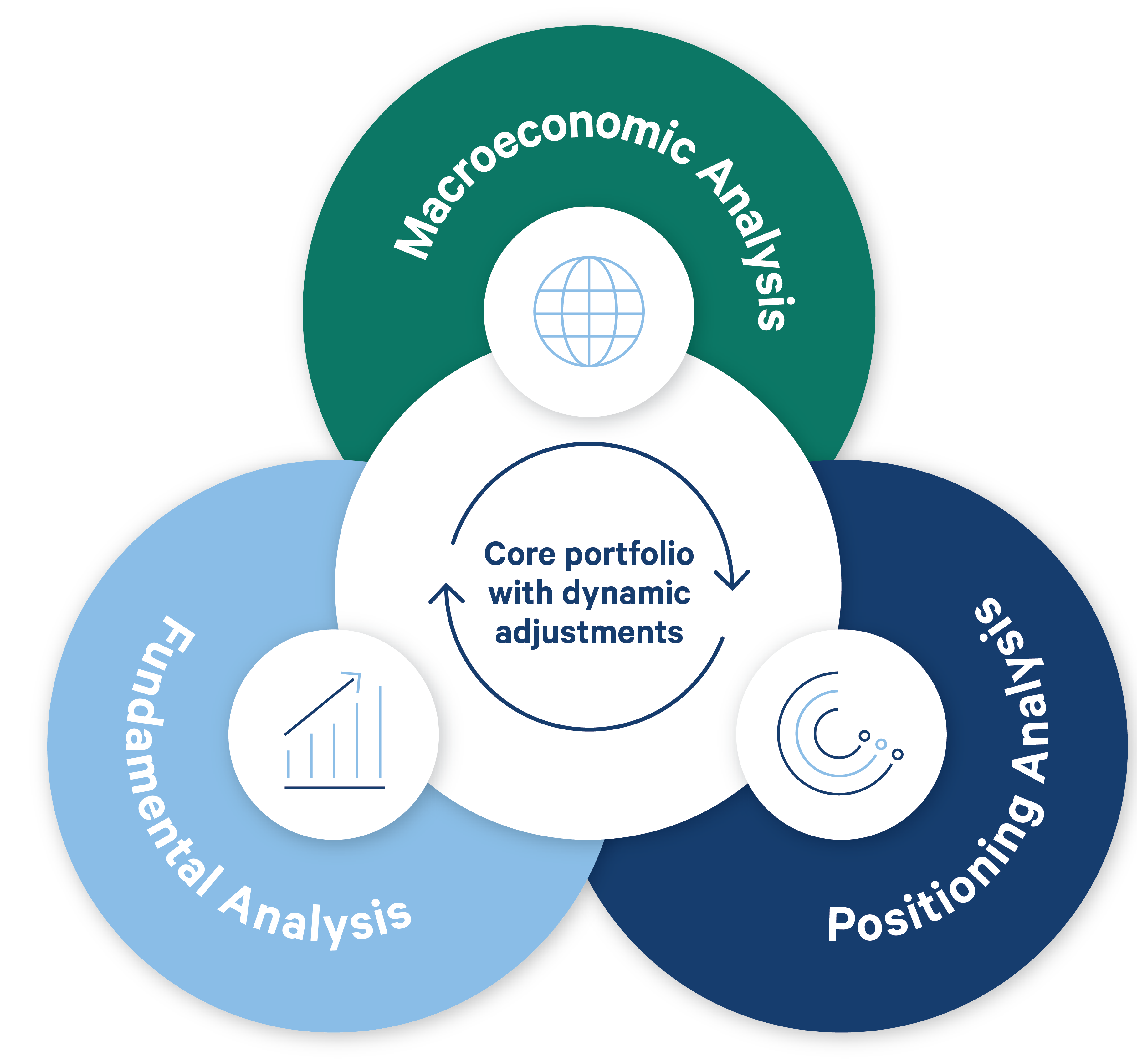

Our proven investment process

The investment process combines a top-down macroeconomic analysis with Wilson Asset Management’s proven fundamental research and market positioning investment process.

Our proven investment process

Board of Directors

Geoff Wilson AO

Chairman

Geoff Wilson has more than 46 years’ direct experience in investment markets having held a variety of senior investment roles in Australia, the UK and the US. Geoff founded Wilson Asset Management in 1997, which today, comprises of 20 investment professionals who offer a combined investment experience of more than 250 years. Wilson Asset Management manages $6 billion on behalf of more than 130,000 investors as the investment manager for nine listed investment companies (LICs) and two unlisted funds: Wilson Asset Management Leaders Fund and Wilson Asset Management Founders Fund. Geoff is currently Chairman of WAM Capital Limited, WAM Leaders Limited, WAM Global Limited, WAM Microcap Limited, WAM Research Limited, WAM Active Limited, WAM Income Maximiser Limited and WAM Strategic Value Limited. He is the founder and Director of Future Generation Australia Limited and Future Generation Global Limited, and Director of WAM Alternative Assets Limited. In 2014 Geoff created Australia’s first listed philanthropic wealth creation vehicles, Future Generation Australia, and subsequently Future Generation Global in 2015. In 2024 Geoff launched Future Generation Women as the first all-female managed fund in Australia, delivering investment returns and advancing economic equality and opportunities for women and their children in Australia. To date, the Future Generation companies have donated $100 million to Australian not-for-profits. Geoff holds a Bachelor of Science, a Graduate Management Qualification and is a Fellow of the Financial Services Institute of Australia and the Australian Institute of Company Directors (AICD). In addition to Geoff’s Directorships with the Wilson Asset Management Group and the Future Generation companies, he also holds Directorships with Staude Capital Global Value Fund Limited (since 2014), Hearts and Minds Investments Limited (since 2018), Sporting Chance Cancer Foundation (since 1997) and the Australian Rugby Foundation (2024).

Kate Thorley

Director

Kate Thorley has more than 26 years’ experience in funds management, financial accounting and corporate governance. Kate is Executive Director of Wilson Asset Management, having served as Chief Executive Officer for 15 years. She is a Director of WAM Capital Limited, WAM Leaders Limited, WAM Global Limited, WAM Research Limited, WAM Active Limited, WAM Microcap Limited, WAM Income Maximiser Limited and WAM Strategic Value Limited. She is also a Director of Future Generation Australia and Future Generation Global. Kate is a Chartered Accountant and a graduate member of the Australian Institute of Company Directors.

Alexa Henderson

Director

Alexa has over 31 years’ global experience in finance, accounting and audit having previously held roles with KPMG, Arthur Andersen and Deutsche Bank (WM Company). Alexa is currently a non-executive director of abrdn UK Smaller Companies Growth Trust PLC, James Walker (Leith) Limited and Chairman of JPMorgan Japan Small Cap Growth & Income PLC.

Melinda Snowden

Director

Melinda has over 30 years’ financial markets experience working as an investment banker with Grant Samuel, Merrill Lynch and Goldman Sachs in Australia and New York. Melinda is Chair of Megaport Limited and a non-executive director of Temple & Webster Group Limited and Brighte Capital Pty Limited. She is a former Chairman of Antares Capital Partners Limited and is a former non-executive director of Sandon Capital Investments Limited, Our Ark Mutual Limited, Mercer Investments (Australia) Limited, MLC Limited, Vita Group Limited, Kennards Self Storage Pty Limited, Newmark REIT Management Limited and Best & Less Group Holdings Limited. Melinda holds a Bachelor’s degree in Economics and Law, as well as a Graduate Diploma in Applied Finance and Investment. She is a Graduate member of the AICD (GAICD) and Fellow of FINSIA.

Dr Ian Langford

Director

Ian holds a Bachelor’s degree in Management, a Master of Arts, a Master of Defence Studies, a Master of Strategic Studies and a Doctor of Philosophy from Deakin University. With 30 years of experience and as a senior officer in the Australian Defence Force, Ian has led large and small teams in complex and ambiguous environments. Ian has held a range of appointments in the Army and Special Forces throughout his career. Ian commanded the 2nd Commando Regiment, as well as multiple Special Operations Task Groups in Afghanistan, Iraq, and on domestic counter-terrorism duties. Ian has also led at the strategic level, responsible for the Army’s future strategic investments, future concepts and capabilities, major capital acquisitions and critical sustainment systems as the Head of Land Capability on two separate occasions in both 2019/20 and again in 2022. Ian has been awarded several Australian commendations, and the Distinguished Service Cross on three occasions. In 2019, he was appointed as an Honorary Aide de Camp to the Governor-General of the Commonwealth of Australia.

Jesse Hamilton

Joint Company Secretary

Jesse is a Chartered Accountant with more than 18 years’ experience working in advisory and assurance services, specialising in funds management. As the Chief Financial Officer, Jesse oversees all finance and accounting of Wilson Asset Management (International) Pty limited. Jesse is currently a non-executive director of the Listed Investment Companies & Trusts Association, Company Secretary for WAM Alternative Assets Limited and WAM Strategic Value Limited and Joint Company Secretary for WAM Capital Limited, WAM Leaders Limited, WAM Global Limited, WAM Microcap Limited, WAM Research Limited and WAM Active Limited, in addition to Future Generation Australia Limited and Future Generation Global Limited. Prior to joining Wilson Asset Management, Jesse worked as Chief Financial Officer of an ASX listed company, and also as an advisor specialising in assurance services, valuations, mergers and acquisitions, financial due diligence and capital raising activities for listed investment companies. Jesse was appointed Joint Company Secretary of WAM Leaders Limited in November 2020.

Linda Kiriczenko

Joint Company Secretary

Linda has over 20 years’ experience in financial accounting including more than 15 years in the funds management industry. As the Finance Manager of Wilson Asset Management (International) Pty Limited, Linda oversees finance and accounting and is also the Joint Company Secretary for six listed investment companies, WAM Capital Limited, WAM Leaders Limited, WAM Global Limited, WAM Microcap Limited, WAM Research Limited and WAM Active Limited. Linda holds a Bachelor of Commerce and is a fully qualified CPA. She is a certified member of the Governance Institute of Australia. Linda was appointed Company Secretary of WAM Leaders Limited in May 2016.

Franked dividends

Our LICs have a proven track record of providing shareholders with a stream of franked dividends.

Diversification

Our LICs offer investors exposure to different market sectors and asset classes through their various underlying investments.

Experienced team

The investment team is comprised of 20 professionals who offer a combined experience of more than 250 years in Australian and international equity markets as well as in alternative assets.

Superior structures

The LIC structure allows us to invest for the long term, without being subject to the impact of applications and redemptions. LICs also adhere to strict corporate governance requirements and act in the best interest of shareholders.

Strong performance

We offer a strong track record of performance based on our rigorous investment process.

Risk-adjusted returns

Our flexible investment mandate allows above-average cash holdings and strong, risk-adjusted returns.

Full market access

We hold over 4,000 company meetings each year, and our knowledge of the market and extensive network continually provides valuable intelligence and investment opportunities.

Transparency & engagement

We provide email updates from our Lead Portfolio Managers and investment team, Chairman and CIO, timely market insights in the form of podcasts, articles and videos, in-person presentations, investor education materials and financial reporting.

Year

Type

- Annual report

- Annual RG 240 update

- Anti-bribery and corruption policy

- Appointment of Wilson Asset Management as Investment Manager

- Chairman's address

- Corporate governance charter

- Corporate governance statement

- Dividend announcement

- Dividend reinvestment plan

- Entitlement offer booklet

- Entitlement offer fact sheet

- Fact sheet

- Financial report

- Independent research report

- Interim financial report

- Investment Approach

- Key dates

- Media release

- Modern slavery statement

- Monthly investment update

- Notice of meeting

- Option prospectus

- Presentation

- Product Disclosure Statement

- Prospectus

- Share purchase plan

- Share purchase plan announcement

- Share purchase plan booklet

- Target market determination

- Term sheet

- Whistleblower policy

- Withdrawal form

Item

- WAM Leaders monthly investment update June 2026pdf

- WAM Leaders Monthly Investment Update May 2026pdf

- WAM Leaders Monthly Investment Update April 2026pdf

- WAM Leaders Monthly Investment Update March 2026pdf

- WAM Leaders Monthly Investment Update February 2026pdf

- Interim FY2026 Key Datespdf

- WAM Leaders FY2026 Interim Financial Reportpdf

- WAM Leaders FY2026 Half Year Resultpdf

- WAM Leaders Monthly Investment Update January 2026pdf

- WAM Leaders Monthly Investment Update December 2025pdf

- WAM Leaders Modern Slavery Statement 2025pdf

- WAM Leaders Monthly Investment Update November 2025pdf

- WAM Leaders Chairman’s Address 2025pdf

- WAM Leaders Monthly Investment Update October 2025pdf

- WAM Leaders Notice of Meeting 2025pdf

- WAM Leaders Monthly Investment Update September 2025pdf

- WAM Leaders Monthly Investment Update August 2025pdf

- WAM Leaders Corporate Governance Charter 2025pdf

- WAM Leaders FY2025 Annual Reportpdf

- WAM Leaders FY2025 Full Year Resultpdf

- WAM Leaders Corporate Governance Statement 2025pdf

- WAM Leaders Monthly Investment Update July 2025pdf

- WAM Leaders Monthly Investment Update June 2025pdf

- WAM Leaders Modern Slavery Statement 2024pdf

- WAM Leaders Monthly Investment Update May 2025pdf

- WAM Leaders Monthly Investment Update April 2025pdf

- WAM Leaders Monthly Investment Update March 2025pdf

- FY2025 Key Datespdf

- WAM Leaders Monthly Investment Update February 2025pdf

- WAM Leaders FY2025 Half Year Resultpdf

- WAM Leaders FY2025 Interim Financial Reportpdf

- WAM Leaders Monthly Investment Update January 2025pdf

- WAM Leaders Monthly Investment Update December 2024pdf

- WAM Leaders Monthly Investment Update November 2024pdf

- WAM Leaders Chairman’s Address 2024pdf

- WAM Leaders Monthly Investment Update October 2024pdf

- WAM Leaders Notice of Meeting 2024pdf

- WAM Leaders Monthly Investment Update September 2024pdf

- WAM Leaders Monthly Investment Update August 2024pdf

- WAM Leaders Corporate Governance Statement 2024pdf

- WAM Leaders Corporate Governance Charter 2024pdf

- WAM Leaders FY2024 Annual Reportpdf

- WAM Leaders FY2024 Full Year Resultpdf

- WAM Leaders Monthly Investment Update July 2024pdf

- WAM Leaders Monthly Investment Update June 2024pdf

- WAM Leaders Monthly Investment Update May 2024pdf

- FY2024 Key Datespdf

- WAM Leaders FY2024 Half Year Resultpdf

- WAM Leaders Monthly Investment Update April 2024pdf

- WAM Leaders Monthly Investment Update March 2024pdf

- WAM Leaders Monthly Investment Update February 2024pdf

- WAM Leaders FY2024 Interim Financial Reportpdf

- WAM Leaders Monthly Investment Update January 2024pdf

- WAM Leaders Whistleblower Policy 2023pdf

- WAM Leaders Monthly Investment Update December 2023pdf

- WAM Leaders Modern Slavery Statement 2023pdf

- WAM Leaders Monthly Investment Update November 2023pdf

- WAM Leaders Monthly Investment Update October 2023pdf

- WAM Leaders Chairman’s Address 2023pdf

- WAM Leaders Monthly Investment Update September 2023pdf

- WAM Leaders Notice of Meeting 2023pdf

- FY2023 Key Datespdf

- WAM Leaders Monthly Investment Update August 2023pdf

- WAM Leaders FY2023 webinar transcriptpdf

- WAM Leaders Corporate Governance Charter 2023pdf

- WAM Leaders Corporate Governance Statement 2023pdf

- WAM Leaders FY2023 Annual Reportpdf

- WAM Leaders FY2023 Full Year Resultpdf

- WAM Leaders Monthly Investment Update July 2023pdf

- WAM Leaders Monthly Investment Update June 2023pdf

- WAM Leaders Monthly Investment Update May 2023pdf

- Strong demand for WAM Leaders Share Purchase Plan and Placement raises over $230 millionpdf

- WAM Leaders Monthly Investment Update April 2023pdf

- WAM Leaders Monthly Investment Update March 2023pdf

- WAM Leaders Share Purchase Planpdf

- WAM Leaders Share Purchase Plan Bookletpdf

- FY2023 Key Datespdf

- WAM Leaders Monthly Investment Update February 2023pdf

- WAM Leaders FY2023 Interim Financial Reportpdf

- WAM Leaders Monthly Investment Update January 2023pdf

- WAM Leaders FY2023 Half Year Resultspdf

- WAM Leaders Monthly Investment Update December 2022pdf

- WAM Leaders Monthly Investment Update November 2022pdf

- WAM Leaders Monthly Investment Update October 2022pdf

- WAM Leaders Notice of Meeting 2022pdf

- WAM Leaders Monthly Investment Update September 2022pdf

- FY2022 Key Datespdf

- WAM Leaders Monthly Investment Update August 2022pdf

- WAM Leaders Monthly Investment Update July 2022pdf

- WAM Leaders Corporate Governance Statement 2022pdf

- WAM Leaders Corporate Governance Charter 2022pdf

- WAM Leaders FY2022 Annual Reportpdf

- WAM Leaders FY2022 Full Year Resultpdf

- WAM Leaders Monthly Investment Update June 2022pdf

- WAM Leaders Monthly Investment Update May 2022pdf

- WAM Leaders Chairman’s Address 2022pdf

- WAM Leaders Monthly Investment Update April 2022pdf

- WAM Leaders Monthly Investment Update March 2022pdf

- FY2022 Key Datespdf

- WAM Leaders Monthly Investment Update February 2022pdf

- WAM Leaders FY2022 Interim Financial Reportpdf

- WAM Leaders Monthly Investment Update January 2022pdf

- WAM Leaders FY2022 Half Year Resultpdf

- WAM Leaders Monthly Investment Update December 2021pdf

- WAM Leaders Whistleblower Policy 2022pdf

- WAM Leaders Modern Slavery Statement 2021pdf

- WAM Leaders Monthly Investment Update November 2021pdf

- WAM Leaders Chairman’s Address 2021pdf

- WAM Leaders Monthly Investment Update October 2021pdf

- WAM Leaders September 2021 Quarterly Reportpdf

- WAM Leaders Notice of Meeting 2021pdf

- WAM Leaders Monthly Investment Update September 2021pdf

- WAM Leaders Monthly Investment Update August 2021pdf

- FY2021 Key datespdf

- WAM Leaders Corporate Governance Statement 2021pdf

- WAM Leaders Corporate Governance Charter 2021pdf

- WAM Leaders FY2021 Full Year Resultpdf

- WAM Leaders FY2021 Annual Reportpdf

- WAM Leaders Monthly Investment Update July 2021pdf

- WAM Leaders Entitlement Offer closes fully subscribed, raising $277.2 millionpdf

- WAM Leaders announce 14.3% increase in FY2022 interim dividend guidancepdf

- Bell Potter research report on WAM Leaderspdf

- WAM Leaders Entitlement Offer Fact Sheetpdf

- WAM Leaders Entitlement Offer Bookletpdf

- WAM Leaders Monthly Investment Update June 2021pdf

- Attractive Entitlement Offer for WAM Leaders shareholderspdf

- Strong outperformance drives increased fully franked final dividendpdf

- WAM Leaders Investment Update May 2021pdf

- WAM Leaders Whistleblower Policy 2021pdf

- WAM Leaders Corporate Governance Statement 2021pdf

- WAM Leaders Corporate Governance Charter 2021pdf

- WAM Leaders Quarterly Planner Report March 2021pdf

- WAM Leaders Monthly Investment Update April 2021pdf

- WAM Leaders Corporate Governance Statement 2020pdf

- WAM Leaders Monthly Investment Update March 2021pdf

- WAM Leaders Modern Slavery Statement 2020pdf

- Bell Potter LIC Weekly Report 8 March 2021pdf

- WAM Leaders Monthly Investment Update February 2021pdf

- WAM Leaders FY2021 Half Year Resultpdf

- WAM Leaders FY2021 Half Year Resultpdf

- WAM Leaders FY2021 Interim Results slidespdf

- WAM Leaders December 2020 Quarterly Planner Reportpdf

- WAM Leaders Monthly Investment Update January 2021pdf

- WAM Leaders Anti-Bribery and Corruption Policypdf

- WAM Leaders Monthly Investment Update December 2020pdf

- WAM Leaders FY2021 Interim Financial Reportpdf

- WAM Leaders Monthly Investment Update November 2020pdf

- WAM Leaders Chairman’s Address 2020pdf

- WAM Leaders Monthly Investment Update October 2020pdf

- WAM Leaders Notice of Meeting 2020pdf

- WAM Leaders Monthly Investment Update September 2020pdf

- Bell Potter Listed Investment Companies Weekly Report – 25 September 2020pdf

- WAM Leaders FY2021 fully franked interim dividend guidance 3.5 cpspdf

- WAM Leaders August portfolio performance & NTA updatepdf

- WAM Leaders Monthly Investment Update August 2020pdf

- FY2021 Key Datespdf

- WAM Leaders FY2020 Annual Reportpdf

- WAM Leaders Share Purchase Plan Bookletpdf

- WAM Leaders Share Purchase Planpdf

- WAM Leaders – Lonsec research reportpdf

- WAM Leaders Monthly Investment Update July 2020pdf

- WAM Leaders FY2020 Full Year Resultpdf

- WAM Leaders Investment Update June 2020pdf

- WAM Leaders Investment Update May 2020pdf

- WAM Leaders Corporate Governance Charter 2020pdf

- WAM Leaders Investment Update April 2020pdf

- WAM Leaders Investment Update March 2020pdf

- FY2020 Key Datespdf

- WAM Leaders Investment Update February 2020pdf

- WAM Leaders FY2020 Interim Financial Reportpdf

- WAM Leaders Investment Update January 2020pdf

- WAM Leaders FY2020 Half Year Resultpdf

- WAM Leaders Investment Update December 2019pdf

- WAM Leaders Whistleblower Policy 2019pdf

- WAM Leaders Investment Update November 2019pdf

- WAM Leaders Dividend Guidance Statementpdf

- WAM Leaders Investment Update October 2019pdf

- WAM Leaders Investment Update September 2019pdf

- WAM Leaders Investment Update August 2019pdf

- WAM Leaders FY2019 Annual Reportpdf

- WAM Leaders Corporate Governance Statement 2019pdf

- WAM Leaders FY2019 Full Year Resultspdf

- WAM Leaders FY2019 Full Year Results pre-releasepdf

- WAM Leaders Investment Update July 2019pdf

- WAM Leaders Investment Update June 2019pdf

- Independent Investment Research June 2019 LMI Updatepdf

- FY2019 Key Datespdf

- WAM Leaders Investment Update May 2019pdf

- WAM Leaders Corporate Governance Charter 2019pdf

- WAM Leaders Chairman’s Address 2019pdf

- WAM Leaders investment update April 2019pdf

- Zenith Annual Report – WAM Leaderspdf

- WAM Leaders March 2019 Investment Updatepdf

- WAM Leaders February 2019 Investment Updatepdf

- WAM Leaders January 2019 Investment Updatepdf

- WAM Leaders FY2019 Interim Financial Reportpdf

- WAM Leaders December 2018 Investment Updatepdf

- WAM Leaders FY2019 Half Year Resultpdf

- WAM Leaders November 2018 Investment Updatepdf

- Ballieu, 3 December 2018pdf

- Baillieu Holst Listed Investment Companies Research – November 2018pdf

- WAM Leaders October 2018 Investment Updatepdf

- Baillieu Holst Listed Investment Companies Research – October 2018pdf

- Baillieu Holst Listed Investment Companies Research October 2018pdf

- WLE September 2018 Investment updatepdf

- Baillieu Holst Listed Investment Companies Research August 2018pdf

- WAM Leaders Corporate Governance Statement 2018pdf

- WAM Leaders FY2018 Annual Reportpdf

- Baillieu June 2018pdf

- Baillieu Holst Listed Investment Companies Research July 2018pdf

- WAM Leaders FY2018 Full Year Resultpdf

- Baillieu Holst Listed Investment Companies Research – June 2018pdf

- June 2018 Investment updatepdf

- WAM Leaders May 2018 Investment updatepdf

- Baillieu Holst Listed Investment Companies Research – May 2018pdf

- WAM Leaders Corporate Governance Charter 2018pdf

- WAM Leaders Chairman’s Address 2018pdf

- Baillieu Holst WLE April 2018pdf

- April 2018 Investment updatepdf

- March 2018 Investment updatepdf

- IIR WLE March 2018pdf

- Baillieu Holst Listed Investment Companies Research March 2018pdf

- February 2018 Investment updatepdf

- WAM Leaders FY2018 Half Year Resultpdf

- January 2018 Investment updatepdf

- WAM Leaders FY2018 Interim Financial Reportpdf

- December 2017 Investment updatepdf

- Baillieu Holst Listed Investment Companies Research – December 2017pdf

- November 2017 Investment updatepdf

- WAM Leaders Chairman’s Address 2017pdf

- October 2017 Investment updatepdf

- WAM Leaders update October 2017 V2pdf

- WAM Leaders update October 2017pdf

- September 2017 Investment updatepdf

- WAM Leaders Dividend Re-Investment Plan Bookletpdf

- August 2017 Investment updatepdf

- July 2017 Investment updatepdf

- WAM Leaders FY2017 Annual Reportpdf

- WAM Leaders Corporate Governance Charter 2017pdf

- Letter to WAM Leaders Optionholderspdf

- WAM Leaders Dividend media releasepdf

- June 2017 Investment updatepdf

- May 2017 Investment updatepdf

- April 2017 Investment updatepdf

- March 2017 Investment updatepdf

- February 2017 Investment updatepdf

- January 2017 Investment updatepdf

- WAM Leaders FY2017 Half Year Resultpdf

- WAM Leaders FY2017 Interim Financial Reportpdf

- December 2016 Investment Updatepdf

- November 2016 Investment updatepdf

- October 2016 Investment updatepdf

- September 2016 investment updatepdf

- August 2016 Investment updatepdf

- July 2016 Investment Updatepdf

- June 2016 Investment Updatepdf

- May 2016 Investment Updatepdf

- WAM Leaders prospectuspdf