The big picture

Ongoing conflict in the Middle East weighed on share markets globally last week. In Australia, the energy sector was the only sector to gain ground, supported by higher oil prices as investors weighed the risk of prolonged supply disruptions through the Strait of Hormuz, a major shipping route for oil, against intermittent signs of potential de escalation. The International Energy Agency announced that it will release 400 million barrels of oil from strategic reserves across its 32 member nations, representing around one third of the group’s total holdings.

Adding to market volatility were concerns about stress in private credit markets, with a number of large private credit funds in the US and Europe restricting redemptions amid expectations of higher default rates, particularly for loans to software companies potentially impacted by artificial intelligence.

Looking ahead, developments in the Middle East and their impact on energy supply are expected to remain key drivers of markets and upcoming interest rate decisions, including in Australia, where the Reserve Bank of Australia (RBA) announces its policy decision tomorrow. All major banks are forecasting a potential rate increase to 4.1%. In the US, the Federal Reserve is widely expected to keep the federal funds rate steady at 3.50%-3.75%. Australian February employment data will also be released, with the economy expected to have added about 20,000 jobs, while the unemployment rate likely edged up to 4.2%.

The RBA’s policy dilemma: Inflation pressures vs. growth risk with Damien Boey

The Reserve Bank of Australia’s March rate decision is finely balanced. The case for more aggressive rate hikes is based on a few arguments: (1) persistent inflation remaining above the Bank’s 2-3% target; (2) policy rules suggesting that the RBA should have been raising rates last year because of capacity tightness; and (3) the risk of inflation pressures broadening out if higher petrol prices feed into wage bargaining claims, or if global supply chain disruptions taking hold.

The case for caution regarding further hikes is based on: (1) high uncertainty and oil prices putting downward pressure on global growth; (2) exchange rate appreciation tightening financial conditions in addition to higher rates; (3) evidence that underlying inflation is cooling from its highs; and (4) the possibility that the supply side of the economy may not be as constrained as the RBA is projecting.

Our view is that the RBA is more likely to take a cautious path. We note that last year, that it thought it might be responding to tightening financial conditions, but in reality it ended up contending with heightened uncertainty. Whether the RBA should respond in the same way to financial conditions shocks versus uncertainty shocks is debatable, in part because uncertainty shocks can dissipate more quickly than financial conditions shocks, forcing the RBA into a more activist mode and away from interest rate smoothing.

An interesting question to ask is whether the RBA would do what it did in 2025 again if it knew it was responding mainly to uncertainty. Knowing the extent of recent public backlash, many would argue no. However, hindsight is a wonderful thing, and the risks are that without perfect foresight, it would not have done things too differently.

Now, the RBA is at risk of responding to an uncertainty shock, but in the opposite direction from what it did in 2025 – responding to upside inflation risk from higher oil prices rather than downside risks to economic growth. If officials do this, they must accept that they are moving away from interest rate smoothing and taking a more activist path. In such circumstances, they also need to be open to cutting rates more quickly if oil prices fall and the economy buckles under the combined weight of higher rates, petrol prices and a stronger currency. We are not so sure that RBA officials are inclined to do so.

To position for what lies ahead, we think that long-duration, high-quality corporate bonds in Australia are attractive. Within equities, we have a bias towards quality exposures that are able to weather some volatility in the cycle.

Stock watch

Ridley Corporation (ASX: RIC), an agriculture inputs distributor, held its 2026 investor day last week. Its FY2026-2028 growth strategy was presented and we visited assets across all divisions. Ridley is well positioned to benefit from structural agricultural tailwinds in Australia. Its recent acquisition of Incitec Pivot Fertiliser (IPF), the largest distributor of fertiliser on the East Coast, also presents a material upside opportunity. Ridley’s scale and management expertise should drive both cost and revenue synergies within IPF. Asset recycling could also support further inorganic bolt on opportunities.

WAM Alternative Assets’ (ASX: WMA) real estate partner Wentworth Capital has recently exchanged on the acquisition of the Novotel and Ibis Hotels in Darling Harbour. Wentworth acquired these two prime hotel assets in one transaction, representing more than 781 rooms across a prime 1.5-hectare landholding in Sydney’s Darling Harbour precinct. Wentworth recently acquired the asset for $390 million, at a discount to comparable Sydney hotel transactions and below estimated replacement cost. The investment provides exposure to a well-recognised, large-scale hotel asset with opportunities to drive income growth through targeted refurbishments and an active management approach. WAM Alternative Assets is positioned to benefit from the site’s longer term redevelopment potential, including the option to add more than 40,000 square metres of additional floor area.

In the media

Upcoming Results Webinars

We have begun hosting the FY2026 Interim Results webinars across our listed investment companies (LICs) and the Future Generation companies.

If you missed them or would like to revisit our previous webinars, you can do so via the links below.

- Watch the WAM Leaders (ASX: WLE) Interim Results Q&A Webinar

- Watch the WAM Income Maximiser (ASX: WMX) Interim Results Q&A Webinar

- Watch the WAM Capital (ASX: WAM), WAM Microcap (ASX: WMI), WAM Research (ASX: WAX) and WAM Active (ASX: WAA) Interim Results Q&A Webinar

- Watch the Future Generation Australia (ASX: FGX) Full Year Results Q&A Webinar.

Webinars this week:

Thursday 19 March 2026 at 10:00am (Sydney time), WAM Global (ASX: WGB) FY2026 Interim Results Q&A Webinar. Register here.

Friday 20 March 2026 at 11:00am (Sydney time), WAM Alternative Assets (ASX: WMA) FY2026 Interim Results Q&A Webinar. Register here.

2026 National Shareholder Presentations

The Wilson Asset Management and Future Generation teams look forward to connecting with shareholders across Australia at the 2026 National Shareholder Presentations. Register here and see below for the event dates.

You asked, we answered

Q. When will WAM Income Maximiser reach the RBA cash rate + 2.5% target income yield?

A. Our target income return, including franking credits, is the RBA cash rate plus 2.5%, which has averaged 6.2% since inception. Based on the annualised March dividend, including franking credits, we have achieved this target income yield on the IPO price within the first 12 months, as set out in the Prospectus. Going forward, we aim to provide investors with a combination of capital growth and income, with the monthly dividend aligned with the target income return.

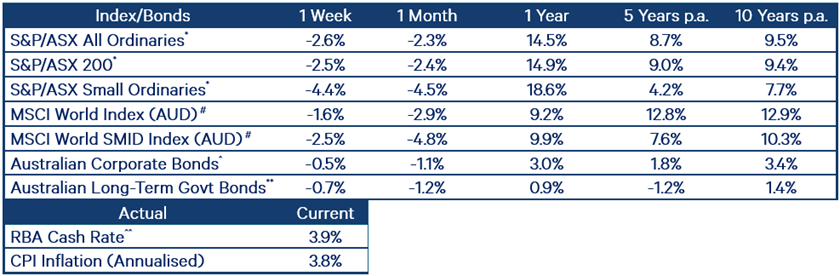

Index returns performance table