The big picture

Australian equities finished the week lower, as gains in the utilities and energy sectors were offset by declines in financials and consumer discretionary stocks. Markets were driven by elevated geopolitical tension and its impact on inflation expectations, with sentiment shifting alongside developments in the Middle East and US-China relations.

The Australian Federal Budget was a key focus for investors, with proposed changes to capital gains tax (CGT), including potential changes to the current 50% CGT discount, alongside adjustments to negative gearing, raising concerns around housing demand, credit growth and broader capital allocation. Chairman and Chief Investment Officer Geoff Wilson and Portfolio Strategist Damien Boey discussed the economic impacts of these changes last week. You can watch their conversation here.

US equity indices ended the week mixed, supported by strong company earnings updates and continued momentum in artificial intelligence (AI) linked sectors. However, the backdrop became increasingly fragile as higher oil prices, firmer inflation, UK sovereign risk and Bank of Japan monetary policy tightening pushed bond yields higher, meaning investors are demanding higher returns for lending money. This reflects growing tension in markets between resilient growth and rising price pressures. The US consumer price index (CPI) rose 0.6% in April, or 3.8% annually, the highest since May 2023, with energy a key driver, underscoring concerns that inflation may be re-accelerating.

The meeting between US President Trump and China’s President Xi meeting renewed focus on Taiwan as a key geopolitical risk, adding to an already uncertain global backdrop.

Looking ahead, markets are likely to remain sensitive to both geopolitical developments and incoming economic data. In the US, key releases include CPI, Purchasing Managers’ Index (PMI) surveys and the Federal Reserve’s meeting minutes, while locally the labour force survey will provide further insight into how the economy is responding to higher interest rates.

The US reporting season has generally been very positive, with the majority of S&P500 companies reporting positive earnings surprises. The results underscore the resilience of corporate America despite investor concerns over the Middle East, higher oil prices and elevated freight costs.

The information technology sector is reporting the highest year over year growth out of any sector led by semiconductors and semiconductor equipment.

The scale of capital being committed to AI infrastructure is the driver. The five largest hyperscalers, Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOG), Meta (NASDAQ: META), and Oracle (NYSE: ORCL) are projected to spend approximately USD 800 billion in 2026. That spending is creating supply-demand imbalances across the hardware supply chain. Specialised hardware including GPUs (Graphics Processing Units), High Bandwidth Memory (HBM), advanced networking gear and power infrastructure are all in short supply. The resulting price increases are flowing through to earnings upgrades for the companies that supply the products most affected by shortages.

The WAM Global investment portfolio has been extremely selective when investing in companies that benefit from this AI infrastructure build-out. This supply-demand dynamic environment will not last forever and our investment process focuses on identifying the world’s best companies with differentiated intellectual property and technological capability that is difficult to replicate. Examples of these companies that reported strong results include ASML (AMS: ASML) semiconductor equipment manufacturer, Taiwan Semiconductor Manufacturing (TSMC) (TPE: 2330) the leading semiconductor foundry, SK Hynix (KRX: 000660) the leading provider of High Bandwidth memory and Quanta Services (NYSE: PWR) critical heavy-duty power infrastructure supplier.

Importantly, our investment portfolio extends well beyond AI hardware. Visa (NYSE: V) reported a strong quarterly report showcasing resilient consumer spending patterns and improved uptake of its value-added services business. RB Global (NYSE: RBA) is taking market share in its auto salvage business and is seeing improved momentum in its marketplace business across commercial, construction, and transportation end markets. The financial exchanges, including Tradeweb (NASDAQ: TW) and Intercontinental Exchange (NYSE: ICE) continue to display attractive compound earnings growth in a fast-changing macroeconomic environment.

Looking ahead, we remain constructive but measured. Corporate fundamentals are robust, but valuations in parts of the market, particularly AI-exposed technology, now embed considerable optimism and we are keeping a close eye on whether the substantial capital being invested in AI translates into commensurate returns. We believe owning high-quality businesses with durable competitive advantages, while being disciplined on valuation, is the most reliable way to navigate this.

In the media: Opposition to the changes to capital gains tax

Stock watch

Macquarie Group (ASX: MQG) recently reported a strong full-year result, with earnings supported by performance across its Commodities & Global Markets (CGM) division, alongside asset realisations and performance fees in Macquarie Asset Management (MAM). The result reinforces the strength of Macquarie’s diversified business model, which combines more stable, annuity-style earnings from Banking & Financial Services (BFS) and MAM with its market-facing businesses that can benefit from periods of increased activity and volatility. We believe this positions Macquarie well to navigate a range of market conditions and continue delivering attractive medium-term growth.

Within the WAM Income Maximiser (ASX: WMX) portfolio, we hold both equity and debt exposures to Macquarie, including the Macquarie Group Limited 6.2302% perpetual callable security (ASX: MQGPG). A callable security gives the issuer the option to repay the security at a future date, providing flexibility around capital management, while investors receive regular coupon payments. As a form of subordinated debt, these securities sit higher than equity in the capital structure, meaning debt holders are paid before shareholders in the event of financial stress. We are attracted to this exposure given Macquarie’s strong balance sheet, disciplined capital allocation and ability to generate earnings across market cycles, which together support a consistent income stream for WAM Income Maximiser.

Portfolios held in: WAM Leaders (ASX: WLE) and WAM Income Maximiser (ASX: WMX)

Qnity Electronics (NYSE: Q) supplies specialty chemicals and advanced materials to the semiconductor industry. The company reported a strong first quarter result, with organic sales increasing 17% year on year and adjusted earnings-per share increasing 33% year-on-year, both ahead of expectations. The company raised its full-year 2026 guidance across all key metrics, reflecting confidence in the underlying momentum. Qnity is well positioned to capitalise on the structural growth in semiconductor demand, particularly as increasing manufacturing complexity drives higher material intensity.

Portfolios held in: WAM Global (ASX: WGB)

You asked, we answered

Q. Have the April NTA’s for all of Wilson Asset Management’s listed investment companies (LICs) been announced?

A. Yes, we released the Monthly Investment Updates for all of our LICs last week, you can view them all here.

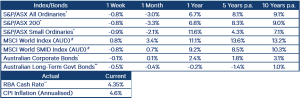

Index returns performance table