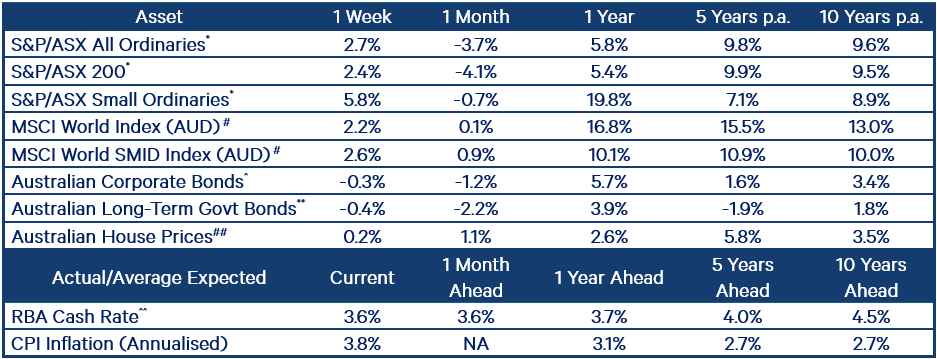

The S&P/ASX 200 Accumulation Index rose 2.4%, led by information technology and materials, with all sectors except energy gaining ground. The S&P/ASX Small Ordinaries Accumulation Index increased 5.8% for the week.

Expectations of a December rate cut have significantly reduced, with some economists flagging a possible hike after Australian consumer inflation accelerated for the fourth straight month in October, up 3.8% year-on-year; the highest in 10 months and above the 3.6% forecast. Trimmed mean inflation also edged up to 3.3% from 3.2% in September.

Treasurer Jim Chalmers and state and territory leaders agreed on regulatory reforms from the Economic Reform Roundtable. Key measures include extending ‘right to repair’ to farm machinery, banning non-compete clauses, streamlining approvals for data centres, and harmonising standards for household electrical goods. Investment in Australian data centres has doubled to $2.8 billion in two months. The Australian Prudential Regulation Authority (APRA) also announced a cap on high debt-to-income lending, limiting banks to 20% of new mortgages where debt-to-income ratios exceeded six times.

In the US, the S&P 500 Index and Small Cap 600 Index gained 3.7% and 4.6% respectively, supported by dovish Federal Reserve comments and weaker economic data that reinforced expectations for a December rate cut. Investors now see an 87% chance of a cut. Tech stocks rebounded on the prior week’s sell off on optimism around artificial intelligence (AI) growth.

Black Friday spending in the US rose 5% from last year, with online sales up 5.3%. The Australian Retailers Association expects Australians to spend a record $6.8 billion, up 4% year-on-year. Global mergers and acquisitions worth US$10 billion or more hit a record 63 deals, driven by US deregulation and easing trade tensions. Donald Trump and Xi Jinping agreed to a one-year trade truce following last month’s summit.

The MSCI World Index (AUD) climbed 2.2% for the week. In the UK, Chancellor Rachel Reeves unveiled a budget raising £26 billion through taxes on gambling, sugary drinks, and high-value properties, including a “mansion tax” on homes over £2 million. The funds will support a £0.50 per hour minimum wage increase (up 4.1%) and an expansion of social welfare benefits.

Tensions escalated between Japan and China after Japanese Prime Minister Takaichi Sanae warned Parliament that a Chinese invasion of Taiwan would be a “survival-threatening situation” justifying use of Japan’s self-defence force. China’s Osaka consul-general responded aggressively.

In commodities, copper gained 4.4% and gold gained 4.3%.

Looking ahead, key data to watch includes US Institute for Supply Management (ISM) manufacturing and services Purchasing Managers’ Index (PMI), European Union inflation, and Australian GDP growth.

Stock watch

Qube Holdings (ASX: QUB)

Qube Holdings, Australia’s largest integrated import and export logistics provider, received a conditional, non-binding proposal from Macquarie Asset Management (MAM) for $5.20 per share, adjusted for any future dividends declared. The proposal represents a 24% premium to the volume-weighted average price (VWAP) since Qube’s FY2025 result and implies an FY2026 enterprise value (EV)/EBITDA multiple of 13.3x. The share price increased by more than 19% on the day of the announcement. Both parties have signed an exclusivity deed granting MAM due diligence until February 2026. Qube’s directors intend to unanimously recommend the deal, subject to conditions including the absence of a superior proposal, which is a possibility given the strategic nature of its assets. Pleasingly for shareholders, Qube’s $400 million franking credit balance may provide scope for increased dividends within the transaction.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

Web Travel Group (ASX: WEB)

Online travel group, Web Travel Group released its result for the first half of FY2026 last week, reporting EBITDA of 4.5%, which was ahead of consensus and Total Transaction Value (TTV) margin at 6.45%, beating guidance of 6.2-6.4%. The company reported a strong $238 million net cash position and $699 million in liquidity, supporting further capital management initiatives following the $150 million buyback completed in the second half of FY2025. Web Travel Group reaffirmed its FY2027 targets of at least a 6.5% TTV margin and around a 50% EBITDA margin, both of which appear achievable given last week’s result and momentum from additional investment in contracting staff. The result has also strengthened confidence in its ability to scale TTV toward its $10 billion FY2030 target. Should Web Travel Group continue to materially outperform the market without sacrificing TTV margin, it would justify an upward re-rating.

Held in: WAM Capital (ASX: WAM), WAM Research (ASX: WAX) and Wilson Asset Management Founders Fund

CTS Eventim (ETR: EVD)

CTS Eventim, Europe’s leading ticketing and live entertainment provider, delivered a strong Q3 FY2025 result with revenue up 3.5% and adjusted EBITDA up 13.8% year-on-year, both ahead of consensus. Margin recovery in live entertainment was a key highlight and management reaffirmed full-year guidance while signalling stronger EBITDA growth than previously guided. Looking ahead, synergies from recent acquisitions and tailwinds from major events like the Winter Olympics should support continued earnings expansion, which we believe will act as a catalyst for the stock and drive an upward re-rating.

Held in: WAM Global (ASX: WGB)

SG Fleet (Intermediate Capital Group)

SG Fleet is the leading provider of novated and corporate fleet leasing in Australia, with a track record of more than 20 years. SG Fleet has a diverse and high-quality customer base with long-standing relationships, and these customers are comprised primarily of government and blue-chip companies. WAM Alternative Assets has exposure to SG Fleet through a loan facility provided by our investment partner Intermediate Capital Group, alongside other lenders. SG Fleet is a strong counterparty for WAM Alternative Assets’ private debt investment, with the company generating stable cash flows in an industry that has been resilient to economic downturns and macroeconomic shocks. We are confident in SG Fleet’s growth potential and ability to service its loan facility, and is backed by Pacific Equity Partners, a highly reputable asset manager with an extensive private equity track record in Australia.

Held in: WAM Alternative Assets (ASX: WMA)

WAM Global insights from China

WAM Global Lead Portfolio Manager Catriona Burns is currently in China meeting companies and local officials across Shanghai, Suzhou, Nanjing, Jurong and Hangzhou, travelling on the high-speed rail network and focusing on property, financials and Local Government Financing Vehicles (LGFVs).

Catriona’s discussions to date have reinforced that China is still managing to grow GDP, supported by rising exports which have been increasingly diverted away from the US, and significant investment in advanced manufacturing and high-tech industries such as electric vehicles, drug innovation, robotics and AI. This should prove sustainable given China’s 15th Five-Year Plan, which will be finalised in March 2026, is expected to emphasise sustainable growth driven by structural reform, an ongoing push towards high-tech manufacturing and domestic consumption.

Within this backdrop we see selective opportunities for WAM Global, while remaining cautious given ongoing property sector pressures and weak consumer sentiment. Key holding Alibaba (BCBA: BABA) is, in our view, a prime beneficiary of the aforementioned tailwinds, given its leadership in cloud, AI and ecommerce.

Index returns performance table