The S&P/ASX 200 Accumulation Index fell 1.3% last week. Gains in materials (+3.8%), energy (+1.9%) and utilities (+1.2%) were offset by losses across information technology (-9.4%) and financials (-4.9%). The S&P/ASX Small Ordinaries Accumulation Index rose 0.4%.

Australia’s unemployment rate fell to 4.3% in October from 4.5% in September, with 43,000 jobs added. This brings the rate back in line with June, July and August. Consumer confidence recorded its first net-positive reading in four years, with optimistic consumers outweighing pessimistic ones. The Liberal Party has joined the Nationals in withdrawing support for Australia’s Net Zero target. Australian beef exports to China rose 67% over the past year to $952 million in the September quarter, while China’s imports of US beef fell 94%.

In the US, the S&P 500 Index edged up 0.1%, while the Small Cap 600 Index declined 1.0%. The longest US government shutdown ended after a spending bill was signed to fund operations through 30 January. The news helped remove major headwinds for markets, however stocks fell on Thursday as questions persisted about how long it will take for conditions to return to normal, amid elevated valuations and increased scrutiny of artificial intelligence spending. Economic data remained a focal point, with the White House representatives indicating that October jobs and inflation reports will be released without the jobless rate.

The MSCI World Index (AUD) declined 0.4%. Switzerland and the US announced a deal to cut tariffs on Swiss imports to the US from 39% to 15%, bringing them in line with European Union levels. In return, Switzerland will invest $200 billion in the US over the next three years. Britain’s unemployment rate rose to 5%, the highest since the pandemic.

In commodities, gold rose 2.1% for the week and remains up 22.4% over the past three months. Copper also gained 2.1% for the week, up 11.1% over three months.

Looking ahead, in the US, Federal Reserve minutes are due, and the Bureau of Labor Statistics will release its September jobs report on Thursday. In Australia, Reserve Bank minutes will be published and quarterly wage growth is expected to rise 0.8% in the third quarter, matching the pace in the second quarter. Flash Purchasing Managers’ Index data will also be released for the Eurozone, the UK, Japan, Australia and India.

Stock watch

CSL (ASX: CSL)

Deputy Portfolio Manager Anna Milne arrived back from CSL’s Capital Markets Days in the US last week. CSL is a global biotechnology company developing plasma therapies, vaccines and treatments for rare diseases. During the trip, Anna met with the management team and toured manufacturing facilities and plasma collection centres in Kankakee, Illinois and Holly Springs, North Carolina. We were encouraged by the additional disclosures on demand drivers for immunoglobulin products and CSL’s initiatives to grow market share, as well as progress in reducing plasma collection and fractionation costs. Overall, we have greater confidence in CSL’s earnings profile and see valuation support at the current share price.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

Navigator Global Investments (ASX: NGI)

Navigator Global Investments (NGI), a diversified alternative asset management company that partners with leading managers, hosted its investor day last week. Investors heard from two partners, 1315 Healthcare and Waterfall AM, who provided strong endorsements of Navigator’s value-add. The company typically acquires 5-25% of a business and brings growth capital, strategic advice and access to the Blue Owl Business Services Platform. Navigator maintains an active and disciplined pipeline of potential new partner firms, targeting managers focused on growth areas such as private equity and real assets. Organic growth from Lighthouse and NGI Strategic, which are targeting EBITDA growth of 5% and 10% per annum respectively, combined with US$80 million of targeted strategic acquisitions across a large opportunity set, position the business to achieve its 2030 goal of doubling EBITDA from 2025.

Held in: WAM Capital (ASX: WAM), WAM Microcap (ASX: WMI), WAM Research (ASX: WAX) and WAM Active (ASX: WAA)

CME Group (NYSE: CME)

CME Group is a leading financial exchange that facilitates trading in futures and options across interest rates, equities, foreign exchange, energy and commodities. The company has benefited from financial market volatility recently and reported solid October operational results, reflecting operational discipline and cost control. Combined, these factors drove an earnings beat in its third quarter result and lower expense guidance for FY2025. The stock is up more than 5% November to date, outpacing the broader market. CME Group is well positioned to capture opportunities in current conditions.

Held in: WAM Global (ASX: WGB)

Sunshine Coast Airport (Palisade Investment Group)

Sunshine Coast Airport (SCA) is a regional airport located in south-east Queensland, serving as the gateway to the Sunshine Coast and Noosa regions. In 2017, our investment partner Palisade Group (Palisade) entered into a binding agreement to lease SCA from the Sunshine Coast Regional Council for 99 years and acquire 100% ownership of the asset. Since the investment, Palisade has significantly enhanced the airport’s value and capacity, completing a $300 million runway extension in 2020, enabling larger aircraft and expanded routes. Palisade has further diversified revenue and strengthened long-term profitability by generating value from non-aviation sources, including initiatives such as optimising car parking, renegotiating rental agreements and leveraging non-aeronautical assets. Palisade continues to implement operational improvements at SCA to unlock further upside and generate a consistent income yield for the WAM Alternative Assets investment portfolio.

Held in: WAM Alternative Assets (ASX: WMA)

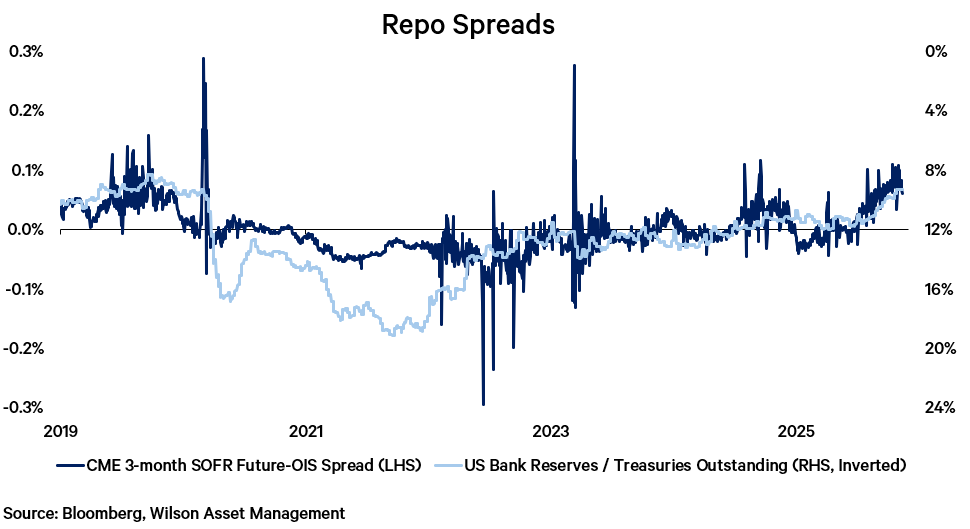

The Fed has the tools to manage plumbing issues this time

Investors are still expressing some concerns about funding markets, even after the US government shutdown ended. Liquidity issues at the end of October have eased, however there are still concerns about what could happen at future month ends. When banks have less cash in the system, the spread or gap between repo (secured) lending rates and risk-free borrowing rates usually widens. Based on this relationship, we should see positive spreads although not as large as what we’ve seen recently. Many commentators, who are inclined towards the view that the Fed needs to do more work to manage spreads, argue that the reason why banks are hoarding liquidity, is that they are sitting on Treasury collateral that has significantly fallen in value since the pandemic as a result of higher rates, whereas official data typically value Treasuries at their original face value.

Fortunately, the Fed stands ready to inject more liquidity if necessary, and is responding to what markets are signalling, rather than theoretical models of where repo rates and “lowest comfortable levels” of liquidity should be. This is all ultimately supportive of risk appetite, but a complication is that the Fed would like to see banks make greater use of standby liquidity facilities between now and year-end, overcoming any stigma attached to using them.

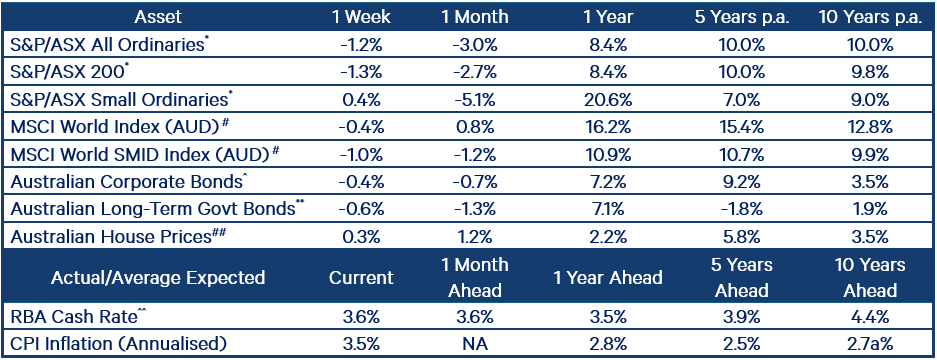

Index returns performance table