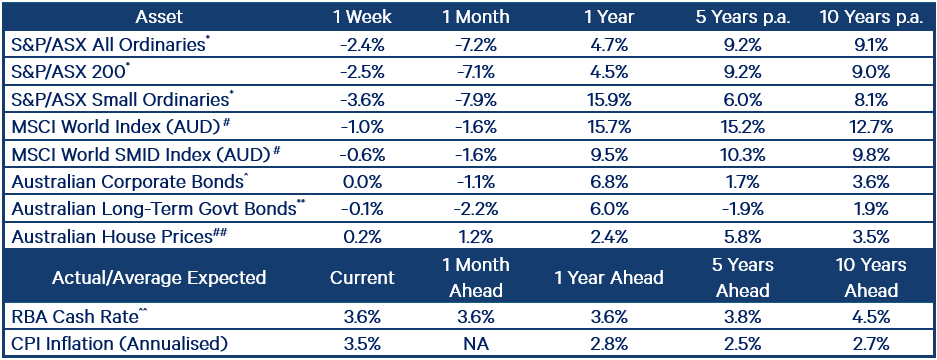

The S&P/ASX 200 Accumulation Index fell 2.4%, with consumer staples the only sector increasing. The S&P/ASX Small Ordinaries Accumulation Index declined 3.6% for the week.

Australian wages rose 3.4% in the 12 months to 30 September, led by public sector growth of 3.8%. Wages are now increasing faster than inflation, which came in at 3.2% over the same period. The Australian Prudential Regulation Authority (APRA) warned that high household debt and rising investor home loan growth are creating vulnerabilities in the banking sector. Australia announced that the US has rolled back tariffs on more than 200 food items, including Australian beef.

In the US, the S&P 500 Index and Small Cap 600 Index fell 1.9% and 1.1% respectively. Attention was on quarterly results from NVIDIA (NASDAQ: NVDA), the largest company in the world, which beat expectations on strong demand for artificial intelligence (AI) chips. The market initially reacted positively, but sentiment turned and the stock finished lower, dragging down major benchmarks. The sell-off appeared to be driven by concerns over elevated valuations; whether AI will deliver enough profits to justify heavy capital expenditure; and Google’s (NASDAQ: GOOG) successful training of the current state of the art, large language model on their own proprietary chips. NVIDIA, Microsoft (NASDAQ: MSFT) and Anthropic also announced a multi-billion-dollar deal for graphic processing units, cloud capacity and AI models.

The US Labor Department’s monthly employment report for September, delayed six weeks by the government shutdown, was released on Thursday and painted a mixed picture. US employers added 119,000 jobs for the month, however, the unemployment rate increased to 4.4% from 4.3% in August, exceeding market expectations of 4.3% and marking the highest level since October 2021. According to CME Group’s (NASDAQ: CME) FedWatch tool, there is nearly a 70% chance the US Federal Reserve (Fed) will cut interest rates at its next meeting, up from 44% a week earlier.

The MSCI World Index (AUD) fell 1.0% for the week. South Korea, the fourth-largest importer of coal and a buyer of $2.4 billion of Australian coal, said it will end all coal power by 2040. Japan and China are involved in an escalating dispute involving Taiwan, with Chinese state media warning citizens not to travel to Japan, and China reimposing a ban on all imports of Japanese seafood. UK inflation eased to 3.6%, down from 3.8% in September, marking the first decline since May.

Looking ahead, we will be watching Australia’s October inflation figures and private capital expenditure. Abroad, the UK Chancellor of the Exchequer, Rachel Reeves will release the long-awaited Autumn Budget, and negotiations are expected to continue between Ukraine and Russia. In the shortened Thanksgiving week in the US, more data delayed by the federal government shutdown will be released.

Stock watch

Charter Hall Group (ASX: CHC)

Charter Hall, an integrated property investment and funds management group, lifted its FY2026 earnings per share guidance by 5.5% to 95 cents at its annual general meeting (AGM) last week, reflecting 17% growth over FY2025. The upgrade was driven by property investment, development income and a stronger outlook for funds under management (FUM) growth. Direct flows are also improving after a muted period. We see the potential for further upgrades from here, particularly as management is incentivised to push the share price to $26 or higher to meet five-year retention bonus hurdles worth potentially more than $100 million. With its dominant market position, Charter Hall is well placed to deploy capital into attractive opportunities as the cycle progresses, supporting further FUM and earnings growth.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

A2 Milk Company (ASX: A2M)

The A2 Milk Company, a producer and marketer of dairy products, held its AGM last week and upgraded FY2026 revenue growth guidance from high single digits to low double digits. The upgrade was driven by strong English label performance as the market recovers through label shifting, innovation, premiumisation and e-commerce growth. The company also outlined transformation activities at its Pōkeno milk processing facility ahead of the transition of its A2 Platinum product in FY2027. The update prompted earnings upgrades by analysts and reinforces its positive momentum.

Held in: WAM Capital (ASX: WAM), WAM Leaders, WAM Income Maximiser and Wilson Asset Management Leaders Fund

Intuit (NASDAQ: INTU)

Intuit, a global financial software company offering tax, accounting, credit monitoring and personal finance products, delivered strong Q1 FY2026 results. Revenue rose 18% and adjusted earnings per share increased 34% year-on-year, both ahead of expectations. The company expects this momentum to continue, guiding for double-digit growth and margin expansion over the next year. We see Intuit as a high-quality business with durable competitive advantages. We believe that it is a long-term beneficiary of AI and that earnings beats over forthcoming quarters will serve as a catalyst.

Held in: WAM Global (ASX: WGB)

Libertas (LVP Private Equity Investments)

Libertas is a market-leading business solutions provider, formed through the merger and integration of three complementary businesses, that specialises in providing advisory, procurement, implementation and managed services solutions across a suite of capabilities utilising SAP SE (NYSE: SAP) software. WAM Alternative Assets co-invested in Libertas alongside our investment partner LVP at an entry valuation that reflects a material discount to businesses of similar scale and diversification to the combined Libertas platform. With SAP SE set to end support for its legacy system in 2027, the resulting mandatory migration cycle to the company’s new S/4HANA Cloud system presents a rare, time-sensitive opportunity for Libertas to capture market share and organically grow revenue, in addition to seeking future acquisition opportunities.

Held in: WAM Alternative Assets (ASX: WMA)

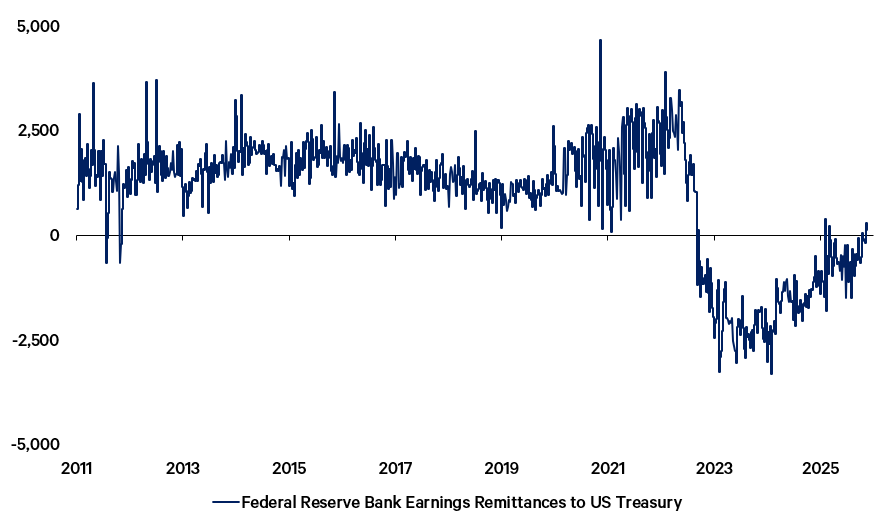

The Fed’s net interest margin is turning positive again

Recently, Fed officials have discussed ending quantitative tightening (QT), with market commentary going one step further to suggest that the Fed needs to expand its balance sheet. Expansion could take one of two forms:

(1) small and occasional security purchases to keep system liquidity ample and ward off money market stresses; or

(2) quantitative easing (QE) to inject large amounts of liquidity into the system on a sustained basis, with a view to lowering long-term bond yields.

The difficulty with QE is that conducting such a program in an environment of elevated inflation risk could undermine the Fed’s credibility and trigger a bond market sell off. A factor undermining the Fed’s credibility with investors is the risk of inflicting losses on itself that end up adding to the US fiscal deficit.

Since the pandemic, the Fed has generally been losing money on its net interest income. It has been paying out large amounts of interest to financial institutions holding excess reserves, while earning less on the coupons from securities it has bought under its past QE programs. Optically, this has been a challenge to conducting QE credibly. However, it now appears that the Fed’s net interest margin is turning positive and it therefore has the credibility to undertake small, occasional security purchases. We think that such a policy move is likely to support investor risk appetite, at least by alleviating concerns about funding markets.

Index returns performance table