The S&P/ASX 200 Accumulation Index declined 1.5% last week, with gains in energy (+1.6%) and consumer staples (+1.4%) offset by declines in healthcare (-8.3%) and information technology (-5.4%).

Australia’s underlying inflation increased for the first time in three years, with trimmed mean inflation at 3.0%, above the expected 2.7%. Australia’s AAA credit rating was reaffirmed by global credit rating agency Fitch, making it one of nine countries rated AAA by all three major credit rating agencies. ASIC confirmed that Bitcoin is unlikely to be considered a financial product. However, products incorporating Bitcoin, such as stablecoins and certain digital wallets, may still be classified as financial products, requiring issuers to hold an Australian Financial Services Licence.

In the US, the S&P 500 rose 0.7% despite seven of its 11 sectors declining, driven by strong results from mega-cap technology companies and continued investment in artificial intelligence. The Small Cap 600 Index fell 2.8% and the MSCI World Index (AUD) ended the week flat.

On Wednesday, the US Federal Reserve cut interest rates by 25 basis points to a 3.75-4.00% range, as widely expected. Chair Jerome Powell stated that another rate cut at the December meeting “is not a foregone conclusion,” noting that the lack of economic data due to the ongoing federal government shutdown may lead to a more cautious approach by policymakers.

The US and China have agreed to a one-year trade truce. The agreement includes a reduction in US tariffs on Chinese imports, a suspension of China’s export controls on rare earth materials and a resumption of Chinese purchases of US soybeans and other agricultural products. While the concessions were modest and leave room for future escalation, the outcome provided temporary relief and supported market sentiment. The US government also announced an $80 billion plan to build nuclear reactors, boosting Australian uranium stocks.

As expected, the European Central Bank kept interest rates unchanged for the third consecutive meeting, with inflation remaining near the 2% target. Japan’s share market reached an all-time high, with the Nikkei 225 Index up more than 27% this year.

Gold declined 2.7% over the week, while iron ore (+1.2%) and aluminium (+0.9%) moved higher.

Looking ahead, key events this week include interest rate decisions in Australia, where investors are pricing in almost no chance of a rate cut given the latest inflation data. Data releases in the US, while limited due to the government shutdown, include ADP employment, the Institute for Supply Management manufacturing and services Purchasing Managers Index reports.

Stock watch

Woolworths Group (ASX: WOW)

Woolworths Group released its Q1 FY2026 sales update last week, showing that the gap in sales growth compared to Coles Group (ASX: COL) narrowed during September and October. This indicates that Woolworths’ recent initiatives are gaining traction, with the share price responding positively to these early signs of recovery. We increased our holding in the company, viewing the valuation gap between the two supermarket retailers as excessive and expecting trading performance to improve as Woolworths begins to cycle through the disruptions experienced over the past year. The upcoming quarter will be a key test of whether the current turnaround strategy is building sustainable momentum.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

Cedar Woods Properties (ASX: CWP)

Cedar Woods, a property developer and investor, reported a strong September quarter reflecting excellent execution, macroeconomic tailwinds, and the ongoing structural housing shortage in Australia. Property settlement volumes rose 17% compared with the same quarter in 2024, and management upgraded FY2026 net profit guidance from 10% to 15% growth. The company has high earnings visibility, with over 90% of FY2026 revenue already pre-sold, the most visibility it has had in decades. With 9,400 lots, dwellings and office units across 35 projects in Queensland, Victoria, Western Australia and South Australia, Cedar Woods is well positioned to benefit from population growth, limited housing supply, and supportive government policy that is expected to sustain demand over the medium term.

Held in: WAM Capital (ASX: WAM), WAM Microcap (ASX: WMI) and WAM Active (ASX: WAA)

Amrize AG (NYSE: AMRZ)

Amrize Ltd, a leading cement and aggregates producer in the US, reported Q3 2025 results last week. Revenue growth of 6.6% came in ahead of expectations and the core business has been robust, despite the tough macroeconomic backdrop, driven predominantly by infrastructure spend and data centres. The company raised full year revenue guidance for 2025, and reiterated its EBITDA and net leverage ratio guidance, which the market received positively. Amrize is set to benefit from a recovery in US residential construction and the ongoing tailwinds from the build-out of data centres supporting artificial intelligence. We view the recent spin-out from Holcim as a positive development given our confidence in the standalone management team’s ability to realise value in the coming years.

Held in: WAM Global (ASX: WGB)

Climate Friendly (Adamantem Capital)

Climate Friendly is a market leader in developing Australian land-based carbon offsets. The business partners with landholders and Traditional Custodians to adopt land management practices that reduce emissions and capture carbon in the land, earning revenue through a fixed fee and a share of proceeds from clients’ generation and sale of Australian Carbon Credit Units (ACCUs). Climate Friendly has a portfolio of approximately 161 active carbon abatement projects that span over more than 10 million hectares of Australian land and have delivered around 23 million tonnes of carbon emission reductions to date. Our investment partner Adamantem Capital invested in the business in March 2021 and achieved a strong early partial exit to Mitsui in May 2022. Climate Friendly management, guided by the expertise of Adamantem, continue to grow earnings and prioritise converting leads in environmental plantings, soil projects and strategic partnerships, and are developing strategies for alternative project growth opportunities.

Held in: WAM Alternative Assets (ASX: WMA)

More evidence of US growth bottoming out during the shutdown period

The longer the US government shutdown persists, the longer investors go without official data on the state of the economy. Nevertheless, private-sector, unofficial data is looking stronger than expected. For example, according to weekly Automatic Data Processing (ADP) data, payrolls growth is bottoming out at rates that are broadly in line with the requirements of a low and stable unemployment rate. Similarly, data from Revelio, feeding into the Chicago Fed’s labour market model, point to a stable unemployment rate in October rather than a rising one. These data points corroborate what regional Fed surveys have been suggesting throughout the shutdown period – that the economy is not sliding into recession just yet. In our view, the reason is that the private sector is starting to do more of the legwork for the economy now that it is becoming less uncertain about the outlook post-Liberation Day. Reinforcing this confidence effect are the willingness of the Fed to make financial conditions easier and benign trade negotiation outcomes in the short term. Interestingly, with regard to the Fed’s decision to cut rates below 4%, we observe a few dissenters, citing a glass half-full view of the economy despite ongoing uncertainty. We think that the current state of play is consistent with higher bond yields and cyclicals outperforming defensives in equities.

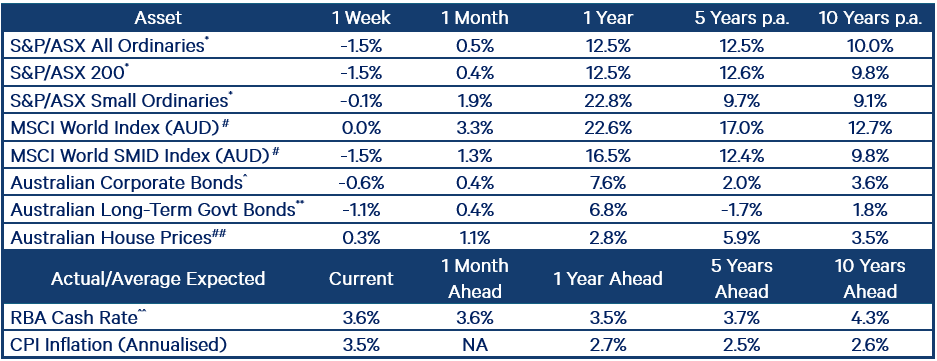

Index returns performance table