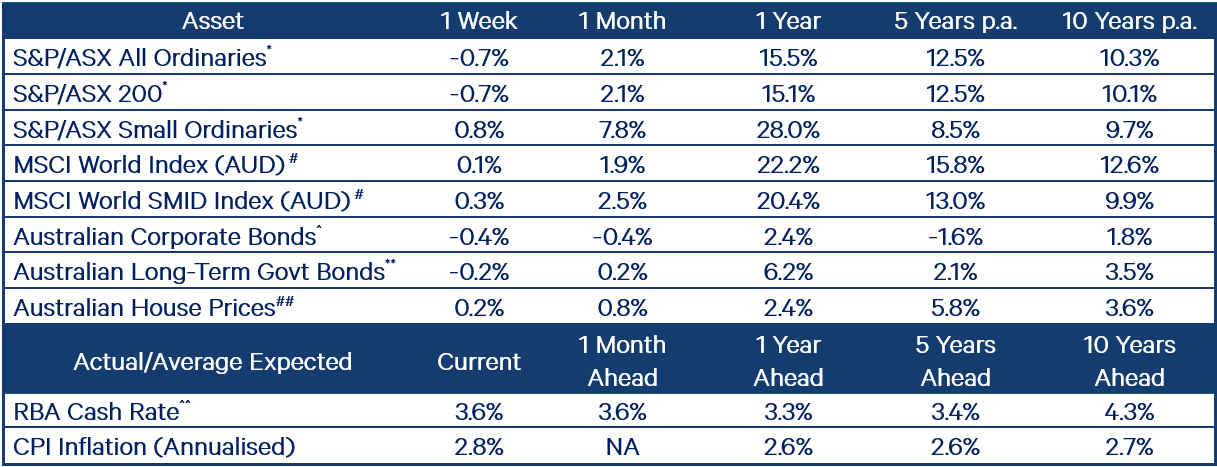

| The S&P/ASX 200 Accumulation Index fell 0.7% last week, with gains in consumer discretionary (+0.4%) and industrials (+0.1%), outweighed by a pullback in all other sectors. The S&P/ASX Small Ordinaries Index performed better, up 0.8%.

Australia’s gross domestic product (GDP) grew 1.8% in the 12 months to June, ahead of forecasts of 1.6% and reducing the likelihood of further near-term interest rate cuts. In the US, the S&P 500 and the Small Cap 600 gained 0.4% and 0.9% respectively over the week. A US jobs report showed just 22,000 jobs were added in August, below the 75,000 expected. Unemployment edged up to 4.3%, the highest since 2021. Markets initially rallied on Friday as weaker jobs data raised hopes of a Federal Reserve rate cut at its next meeting, however sentiment later reversed on concerns that rate cuts alone may not be enough to boost economic growth. Earlier in the week, consumer spending data showed resilience, with July recording the strongest monthly increase in four months. Markets are now nearly fully pricing in at least a 0.25% rate cut at the Fed’s next meeting with US bond yields slipping to the lowest level since April. Meanwhile, gold rallied to a new all-time high of US$3,587/oz. A US Appeals Court ruled that most of Trump’s tariffs are illegal but allowed them to remain in place until 14 October while the Administration appeals the decision to the Supreme Court. The MSCI World Index (AUD) rose 0.1% for the week. In Europe, headline inflation in the eurozone edged up to 2.1% in August, close to the European Central Bank’s (ECB) 2% medium-term target. Core inflation was steady at 2.3%, while services inflation eased slightly to 3.1% from 3.2% in July. Comments made by ECB policymakers reinforced expectations that rates are likely to remain unchanged in September and stay on hold for some time. In France, a confidence vote in Prime Minister François Bayrou’s government is scheduled for 8 September, as it seeks to pass the proposed €44 billion deficit-reduction plan. Looking ahead, key data releases include US consumer price inflation (expected at 2.9% year on year), as well as Australian consumer and business confidence figures. Inflation data from China and India, the ECB’s rate decision and potential economic policy announcements from senior Chinese officials will also be in focus. Stock WatchQantas (ASX: QAN)Last week, we met with the management team from Qantas, Australia’s largest domestic and international airline. Qantas recently reported a solid FY2025 result, with profit before tax up 15% year on year, demonstrating that the dual-brand strategy is working well and that its Loyalty business continues to deliver double-digit growth. Our discussion with management gives us further confidence in the medium-term outlook, with a supportive industry backdrop where rational competition and resilient travel demand are driving capacity and revenue per available seat kilometre (RASK) growth, more than offsetting cost inflation. Management also expressed confidence in the successful delivery of Project Sunrise, Qantas’ plan to operate ultra-long-haul non-stop flights, which will scale its international business. We continue to like the story given Qantas’ dominant market position and strategy execution, and see further upside to both earnings and valuations. Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund COG Financial Services (ASX: COG)COG Financial Services, Australia’s largest aggregator of finance brokers and equipment leasing businesses, has announced the $40 million acquisition of EasiFleet, a salary packaging and novated leasing business. The acquisition is a good strategic fit, expanding COG’s scale and geographic reach in novated leasing while adding complementary customer exposure across its existing brand portfolio. COG has already been growing strongly in this segment, with FY2025 profit before tax from novated leasing up 22% on the prior year. The acquisition is expected to be high single-digit earnings accretive and was completed at an attractive valuation multiple below where peers are trading. While cyclical factors have weighed on COG’s recent earnings, we continue to see long-term upside as management executes a more focused strategy, with the AGM the next potential catalyst. Held in: WAM Capital (ASX: WAM), WAM Microcap (ASX: WMI), WAM Research (ASX: WAX), WAM Active (ASX: WAA) and Wilson Asset Management Founders Fund Alibaba (NYSE: BABA)Alibaba Group, China’s largest e-commerce and cloud services company, recently reported a strong 1Q FY2026 update, including higher-than-expected cloud revenue growth and record quarterly capital expenditure despite ongoing foreign chip constraints. Management noted it is working to materially improve food delivery and quick commerce (ultra-fast delivery) unit economics over the coming months, while maintaining confidence in sustaining advertising revenue growth momentum for the remainder of FY2026. The result has strengthened visibility around Alibaba’s position as China’s leading cloud hyperscaler and supports the renewed narrative for Alibaba Cloud’s long term growth prospects. Held in: WAM Global (ASX: WGB) AgriBio (Palisade Group)AgriBio (formerly the Biosciences Research Centre) is Australia’s first integrated agricultural systems biology hub, a 33,000m² state-of-the-art facility at La Trobe University in Melbourne. Fully operational since 2012 under a 25-year public–private partnership with the Victorian Government and La Trobe, it accommodates around 400 staff and students and is the centrepiece of Victoria’s agri-research ecosystem. The facility drives innovation in plant and animal technologies and biosecurity, underpinned by long-term CPI-linked availability payments from the State of Victoria that deliver stable, government-backed cashflows. WAM Alternative Assets’ investment partner Palisade Group owns 49.9% of the asset and sits on the board of directors, protecting investor interests. Held in: WAM Alternative Assets (ASX: WMA) FY2025 Full Year Results and Webinars

|

Upcoming Wilson Asset Management events

Upcoming Wilson Asset Management events