The S&P/ASX 200 Accumulation Index rose 0.2% last week, supported by strong gains in the materials sector (+5.9%), while the Small Ordinaries Index rose 0.8%.

The Monthly Consumer Price Index (CPI) for August showed an annual increase of 3.0% over the 12 months to August, up from 2.8% in July and slightly above expectations of 2.9%. The result sits at the top of the Reserve Bank’s 2-3% target inflation range, with economists expecting the RBA to keep rates on hold tomorrow (Tuesday).

In the US, the S&P 500 and S&P SmallCap 600 declined 0.3% and 0.6% respectively, while the MSCI World Index (AUD) gained 0.3%. Hawkish commentary from some Federal Reserve officials signalled a slower pace of monetary easing than investors had anticipated, with Fed Chair Jerome Powell highlighting near-term upside inflation risks and downside labour market risks.

The US Government announced 100% tariffs on imports of branded or patent-protected drugs from companies that are not building manufacturing plants in America, effective 1 October 2025. Initial concerns for Australia’s $2.2 billion in pharmaceutical exports eased after CSL (ASX: CSL), Telix Pharmaceuticals (ASX: TLX) and Clarity Pharmaceuticals (ASX: CU6) confirmed they operate US-based facilities.

Lithium Americas Corp (LAC), owner of the US’ largest lithium mine, increased 80% after the US government announced it would take a 10% stake in the company. The news supported local lithium producers, with Pilbara Minerals (ASX: PLS), Liontown Resources (ASX: LTR) and Mineral Resources (ASX: MIN) all rallying. Brent crude oil rose 5.2% for the week after President Trump urged European Union nations to end Russian oil and gas imports, boosting energy stocks. President Trump also announced further tariffs, including 25% on heavy-duty trucks and 30-50% on furniture.

Looking ahead, key events this week include the RBA’s policy decision (Tuesday), US labour market data providing insight into employment conditions after last month’s weak report and Chinese Purchasing Managers’ Index (PMI) releases, which will offer a read on September economic activity.

Stock Watch

Rio Tinto (ASX: RIO) and BHP (ASX: BHP)

Diversified miners Rio Tinto and BHP saw share prices rise amid copper supply disruptions and higher prices. Copper gained 3.1% last week following a mudslide at Indonesia’s Grasberg mine, the world’s second-largest copper mine, temporarily halting operations. Freeport-McMoRan, the mine’s owner, declared force majeure and lowered its 2025 sales forecasts, with 2026 output potentially 35% below pre-incident estimates. Supply concerns were further compounded by Hudbay Minerals (TSE: HBM) temporarily shut down a mill at its Constancia mine in Peru due to political protests. Unplanned supply disruptions now account for an estimated 5.7% of global copper production, highlighting long-term supply constraints and supporting the outlook for producers such as Rio Tinto and BHP.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

Tuas (ASX: TUA)

Tuas, a provider of mobile and broadband telecommunications services (formerly TPG Singapore), reported its FY2025 results last week. Revenue grew 29%, earnings before interest, taxes, depreciation and amortisation (EBITDA) increased 38% and margins expanded to 45% from 42% last year. The uplift was driven by a growing subscriber base and a broader plan mix catering to different customer needs. As at 31 July, Tuas reported 1.254 million subscribers, up 19% year-on-year. Management noted that FY2026 has begun with continued momentum across both mobile and fibre broadband, underpinned by ongoing expansion. The company remains focused on margin optimisation and disciplined cash management, while investing to grow its subscriber base and expand 5G coverage. We believe Tuas is well placed to continue its growth trajectory over the next three to five years.

Held in: WAM Capital (ASX: WAM), WAM Leaders, WAM Research (ASX: WAX), WAM Microcap (ASX: WMI), WAM Global (ASX: WGB), WAM Income Maximiser, Wilson Asset Management Leaders Fund and Wilson Asset Management Founders Fund

Quanta Services (NYSE: PWR)

Quanta Services is a leading specialised contracting services company that provides infrastructure solutions across the utilities, renewable energy, pipeline and energy industries. Since 2015, the company has delivered exceptional earnings growth (approximately a 25% compound annual growth rate), driven by best-in-class execution and strategic expansion. Quanta has the potential to double its total addressable market through its expansion into data centres, with recent platform acquisitions Cupertino Electric and Dynamic Systems enabling it to sustain consistently high-teens earnings growth over the next decade. Quanta’s diversified markets and proven execution make the current share price an attractive entry point relative to broader engineering and construction peers.

Held in: WAM Global

BINGO Industries (Intermediate Capital Group)

BINGO Industries is the largest vertically integrated building and infrastructure (B&I) waste operator in New South Wales and Victoria – the two largest states by waste volume. BINGO provides B&I collection and recycling services, with a dominant position in the NSW market. BINGO’s competitive advantage is supported by the largest collection fleet in NSW and a large-scale post-collection network situated in strategic locations, within a capital-intensive industry with high barriers to entry. WAM Alternative Assets, via its investment partner Intermediate Capital Group, provides financing to BINGO via a senior secured loan and benefits from BINGO’s strong earnings and cash flow generation, which are underpinned by the company’s efficient recycling facilities and its ability to pass through cost increases.

Held in: WAM Alternative Assets (ASX: WMA)

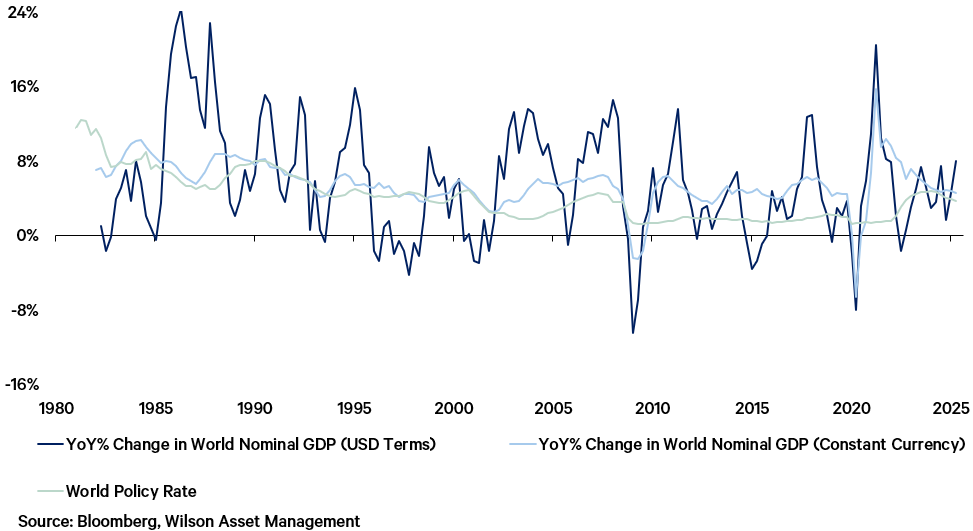

Global rates are meaningfully below growth and inflation

We often focus on debates about whether Australian or US policy settings are appropriate for prevailing macroeconomic conditions. However, it is also worthwhile to consider the appropriateness of global rate settings. A simple way to judge this is to compare how weighted average policy rates are tracking relative to nominal gross domestic product (GDP) growth. Currently, the GDP-weighted global policy rate sits at 3.7%. However, in US dollar terms, world nominal GDP is up by 8% in the year to Q2. Stripping out currency movements, world nominal GDP growth is 4.5%. Either way, global rates are below nominal GDP growth, consistent with easy financial conditions. Pessimistic investors will argue that global growth is slowing, and that, in a year or so, policy rates will be appropriate for evolving macroeconomic conditions. Conversely, we highlight that rates are already 0.8% too low and we can see scenarios where global growth reaccelerates. Historically, whenever global policy rates sit below global nominal GDP growth, we tend to see commodity prices rise shortly after. Further, there are risks that if rates move too far below nominal GDP growth, bond yields could rise at some point, as investors see an end to easing cycles and even ponder future rate hikes. For retail investors, this backdrop can favour equities and commodities but argues for caution on long-duration bonds – making diversification a prudent strategy.

FY2025 reporting season: insights from the investment team

This reporting season was described as one of the most volatile in history, delivering sharp swings in share prices as companies either exceeded or fell short of analyst’s expectations. Against this backdrop, our large cap, small to mid-cap and global investment teams shared their views on standout performers, disappointments and the broader economic signals that emerged from results. You can watch their recap of the reporting season that was, here.

Upcoming Wilson Asset Management Events

October Shareholder Presentations

The Wilson Asset Management and Future Generation teams look forward to meeting with shareholders at our upcoming Shareholder Presentations in October. Meet the Wilson Asset Management investment team to hear their market outlook, high-conviction stock picks and discuss some of the key themes influencing the investment portfolios. Learn more about the Future Generation companies and how they invest for impact, delivering both investment and social returns for shareholders.

Register using the following links:

Newcastle | Thursday, 16 October 2025

Gold Coast | Tuesday, 21 October 2025

Toowoomba | Wednesday, 22 October 2025

Noosa | Thursday, 23 October 2025

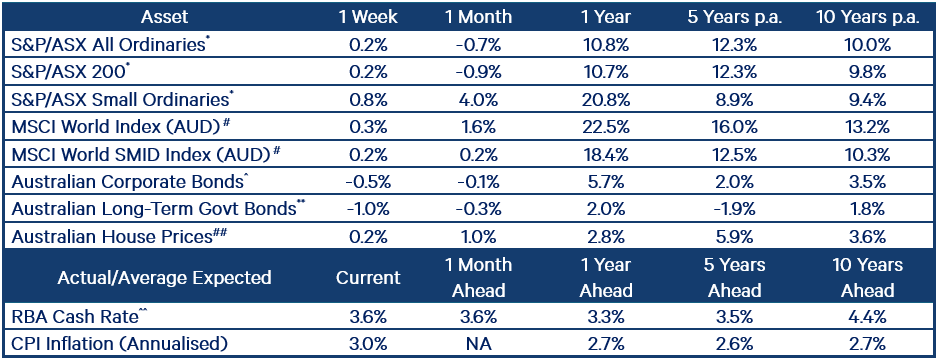

Index returns performance table