The S&P/ASX 200 Accumulation Index increased 0.4% last week, driven by gains in materials (+4.0%), real estate (+1.7%) and healthcare (+1.3%). The Small Ordinaries Index declined 0.5%.

Australia’s unemployment rate increased to a four-year high of 4.5%, slightly above the 4.3% priced in by market expectations. This lifted expectations for a November interest rate cut to around 70%. Prime Minister Anthony Albanese is expected to announce a major critical minerals agreement with the US during his meeting with President Trump on Monday (Tuesday AEDT). The deal could strengthen supply chains for materials used in smartphones, turbines and defence equipment, reducing US reliance on China.

In the US, the S&P 500 and SmallCap 600 both rose by 1.7% and 3.0% respectively, while the MSCI World Index (AUD) gained 1.4%. Markets began the week positively after US and Chinese officials appeared to walk back some of the prior week’s trade tensions, further supported by Federal Reserve (Fed) Chair Jerome Powell signalling that the central bank remains on track to cut short-term interest rates again this year. US earnings season began with several major banks reporting better-than-expected Q3 FY2025 results. Markets softened on Thursday after two regional banks disclosed loan issues involving alleged fraud, raising concerns about credit risk and the broader health of the regional banking sector. National Economic Council Director Kevin Hassett downplayed the concerns, stating that the sector has “ample reserves.”

President Donald Trump said Indian Prime Minister Narendra Modi indicated India would stop buying Russian oil, potentially easing trade tensions between the US and India. India currently faces 50% tariffs on many exports to the US.

Gold prices continued to rise, gaining 3.6% over the week and climbing nearly 28% over the past three months.

Key events we are monitoring this week include Purchasing Managers’ Index (PMI) data for Australia, Europe, the UK and India; Q3 gross domestic product (GDP) data from China; and the US federal government shutdown, which is looks set to enter its fourth week.

Stock Watch

Telix Pharmaceuticals (ASX: TLX)

Telix Pharmaceuticals is a global commercial-stage biopharmaceutical company focused on developing and commercialising therapeutic and diagnostic radiopharmaceuticals and related medical technologies. The company reported its Q3 2025 results last week, surprising the market with an upgrade to full-year revenue expectations. While there had been concerns about a potential funding gap following reimbursement changes, these were more than offset by stronger product volumes. We built a position in Telix primarily on valuation grounds, with the current diagnostics business valued at around $15 per share, implying limited value is being ascribed to its therapeutics pipeline. Telix’s share price closed at $16.65 on Friday.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

SRG Global (ASX: SRG)

SRG Global, an Australian diversified infrastructure services company operating across maintenance, industrial services, engineering and construction, has agreed to acquire 100% of Total AMS Pty Ltd (TAMS), a privately owned national service provider to the marine infrastructure sector. The acquisition includes an upfront payment of $85 million and a two-year earn-out, under which vendors will receive 100% of TAMS’ incremental annual earnings before interest, taxes, depreciation and amortisation (EBITDA) between $30 million and $40 million, and 50% of incremental EBITDA above that level. TAMS is forecast to deliver $35 million in EBITDA and is forecast to be 25% earnings accretive to SRG Global, with further upside potential from any outperformance. We view the acquisition as compelling both in terms of valuation and strategic rationale and see additional opportunities for SRG Global through ongoing earnings growth and future merger and acquisition activity. SRG Global warrants a valuation premium to peers given its strong management track-record and above-peer-group average profitability and earnings growth.

Held in: WAM Capital (ASX: WAM) and WAM Active (ASX: WAA)

LVMH Moët Hennessy Louis Vuitton SE (EPA: MC)

Luxury goods provider LVMH Moët Hennessy Louis Vuitton SE (LVMH) reported last week that its Q3 FY2025 results beat expectations. This was driven by higher volumes and traffic in its largest divisions, Fashion and Leather Goods, Watches and Jewellery and Selective Retailing, with the strongest improvements seen in China, Southeast Asia and the US. While the broader sector continues to navigate uncertainty, LVMH’s results highlight that actions taken to revitalise its key Fashion and Leather Goods brands are delivering results. We believe the underlying improvement in sales will ultimately drive margin stabilisation and renewed earnings growth, acting as a catalyst to drive the share price.

Held in: WAM Global (ASX: WGB)

Eastwood Private Hospital (Barwon Investment Partners)

The Eastwood Private Hospital is one of South Australia’s leading health infrastructure developments aimed at addressing growing demand for medical services. Construction on the Eastwood Private Hospital commenced in September 2023, with the project achieving practical completion in April 2025. The property, which has been fully pre-leased to Eastwood Private Hospital on a 15-year triple net lease (a commercial lease agreement where the tenant pays the base rent plus three “nets”: property taxes, insurance, and maintenance costs), offers a dedicated short-stay facility for surgical patients with 51 inpatient beds and six operating theatres. It is expected to treat more than 7,000 patients each year. WAM Alternative Assets gains access to this institutional-quality healthcare real estate asset through our investment partner Barwon Investment Partners.

Held in: WAM Alternative Assets (ASX: WMA)

Salter Brother Emerging Companies (ASX: SB2)

Salter Brothers Emerging Companies is a listed investment company (LIC) that invests in small-cap companies with a market capitalisation of less than $500 million. Last week, we increased our substantial position as part of our strategy to accumulate shares opportunistically when the discount to net tangible assets (NTA) is compelling and there is a catalyst. The LIC commenced paying dividends in CY 2025 and is currently yielding more than 8% per annum, including franking. We see several catalysts that could drive further shareholder returns from here and help narrow the share price discount to NTA.

Held in: WAM Strategic Value (ASX: WAR)

The US economy remains resilient in the face of the ongoing government shutdown and tariff concerns

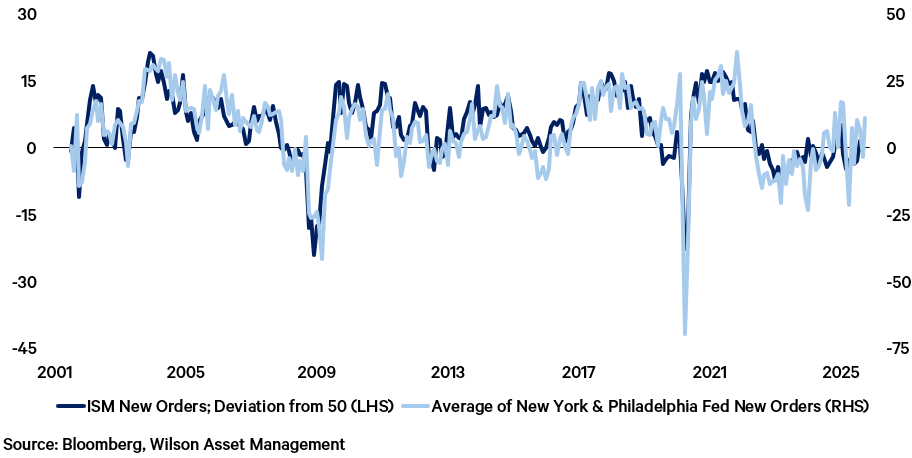

There is a lack of current official US economic data due to the prolonged government shutdown. Many investors are of the view that recession risks increase the longer the shutdown continues, especially now that tariff uncertainty is returning. However, many Fed and private-sector surveys continue to be published in the absence of official data that suggests otherwise. From the New York and Philadelphia Fed October surveys, we see indications that economic growth may actually be improving, with new orders indices having returned to expansionary territory. Given the historically strong correlation between the new orders components of regional Fed surveys and the Institute for Supply Management (ISM) survey, and given that the ISM New Orders Index is a timely leading indicator of corporate earnings, these surveys bode well for the US economy. Notably, the survey shows signs of building pipeline inflation pressures, because order backlogs are no longer shrinking and tariffs continue to filter through. This warrants close monitoring for bond yields and valuations

WAM Income Maximiser Share Purchase Plan

The WAM Income Maximise Board of Directors has announced a Share Purchase Plan (SPP) to eligible shareholders1. The SPP provides the opportunity to acquire up to $30,000 of fully paid ordinary shares in WAM Income Maximiser at a discount to the current share price2, without incurring brokerage fees. Shareholders who participate in the SPP will be eligible to receive the November and December 2025 monthly fully franked dividend with guidance3 of 0.35 cents per share and 0.40 cents per share respectively. The SPP will be offered to eligible shareholders1 at the lower of:

- $1.602 per share4 equal to the Company’s 30 September 2025 pre-tax net tangible assets (NTA), less the October 2025 fully franked dividend; or

- a 2.5% discount to the 5-day volume-weighted average price (VWAP) at the issue date of 17 November 2025.

Shareholders will have the opportunity to apply for the SPP via an online acceptance facility that is now open and closes on Wednesday 12 November 2025 at 5:00pm (Sydney time). Full details including access to the dedicated website and application instructions are available in the SPP booklet which was announced earlier on Friday.

WAM Income Maximiser Chairman Geoff Wilson AO, Lead Portfolio Manager Matthew Haupt and Portfolio Strategist Damien Boey, will host a webinar on Wednesday 29 October at 11:00am (Sydney time) to provide information on the SPP and an investment portfolio update. You can register for the webinar and submit questions here.

Upcoming Wilson Asset Management Events

October Shareholder Presentations

The Wilson Asset Management and Future Generation teams look forward to meeting with shareholders at our upcoming Shareholder Presentations in Queensland this week.

There are limited spaces remaining. Register using the following links:

Gold Coast | Tuesday, 21 October 2025

Toowoomba | Wednesday, 22 October 2025

Noosa | Thursday, 23 October 2025

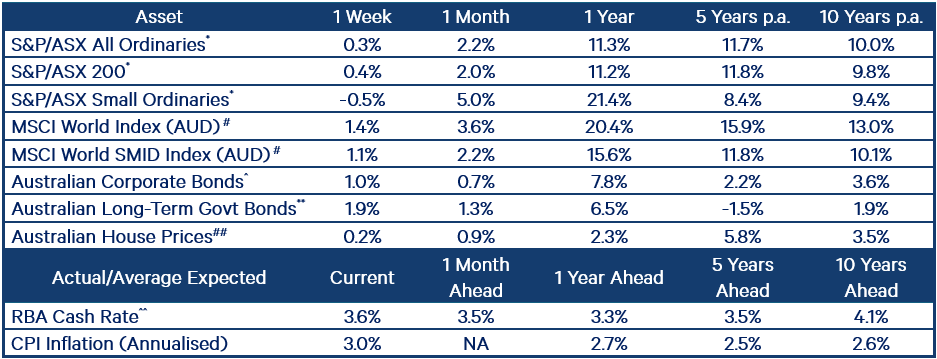

Index returns performance table