The S&P/ASX 200 Accumulation Index rose 0.3% last week, led by a 5.4% gain in the energy sector and supported by a 7.1% rise in Brent oil prices. Oil strengthened after the US imposed sanctions on Russia’s two largest oil companies, citing Moscow’s “lack of serious commitment” to ending the war in Ukraine and urging an immediate ceasefire. The Small Ordinaries Index fell 1.0%.

In the US, the S&P 500 and Small Cap 600 indexes rose 1.9% and 3.0% respectively, while the MSCI World Index (AUD) gained 1.4%. Despite the ongoing US government shutdown, the Bureau of Labor Statistics released September inflation figures with both headline and core inflation coming in at 3.0%, slightly below expectations. Leading indicators point to inflation of 3-4% with the upper end including the University of Michigan survey. Early readings from the S&P Global purchasing managers’ indices (PMIs) suggest business activity strengthened in October. In the UK, core inflation eased to 3.5% down from 3.6% in August, increasing markets’ expectations of a rate cut in December.

After two days of talks in Malaysia, Chinese officials said the US and China had reached a preliminary consensus on issues including export controls, fentanyl, and shipping levies. Chinese government data showed that its economy grew 4.8% year-on-year in the September quarter, slightly above expectations but marking its slowest pace in a year, as the property downturn and US trade tensions continued to weigh on demand.

Gold prices fell 3.3% over the week, including a 6% drop on Wednesday, the largest intraday fall since 2013. Silver also declined nearly 9% the same day. The sell-off reflected profit-taking after strong year-to-date gains and higher margin requirements in Shanghai, which triggered further selling and tighter physical supply.

Looking ahead, key events this week include monetary policy decisions from the EU, Japan, and Canada, and the US Federal Reserve’s Federal Open Market Committee meeting

Stock Watch

Woodside Energy (ASX: WDS)

Global energy company Woodside Energy reported Q3 FY2025 production ahead of market expectations, supported by strong performance at its Pluto and Sangomar assets. The company upgraded its 2025 production guidance and lowered its unit operating cost guidance with a largely fixed operating base. During the week, Woodside also announced the sale of a 10% interest in Louisiana LNG LLC and an 80% interest in Driftwood Pipeline LLC to Williams Companies Inc. (NYSE: WMB) for US$378 million. The market responded positively, as the sale suggests Woodside has added value to the project connecting Louisiana LNG to other North American gas pipelines over the past year. The sale implies a value of approximately A$2 per share for Woodside’s remaining 90% stake, above expectations. The transaction also reduces total net capital expenditure for the Louisiana LNG Project to US$9.9 billion (down from US$11.8 billion), further improving the company’s gearing outlook, which has already benefited from production upgrades and delayed capex this year. With the potential for further sell-downs and first LNG output from the Scarborough project on track for H2 FY2026, the outlook for Woodside remains compelling.

Held in: WAM Leaders (ASX: WLE) and Wilson Asset Management Leaders Fund

Pinnacle Investment Management (ASX: PNI)

Pinnacle Investment Management, a multi-affiliate investment firm, reported $13 billion in net inflows for the September quarter, including record retail and wholesale flows, and near-record contributions from domestic institutional and offshore clients. Pinnacle also announced an investment in Advantage Partners, a mid-market Japanese buyout manager. This marks Pinnacle’s first expansion into Asia and its 19th affiliate. Advantage is expected to more than double its assets over the coming year. Pinnacle has entered into a global distribution agreement with Advantage, which will not only benefit the manager but also enhance Pinnacle’s opportunity to grow flows from Japan across other affiliates. Pinnacle has a track record of partnering with high-quality managers and fostering growth in adjacent strategies. We see a growing runway for Pinnacle as it continues to expand offshore and believe there remains valuation upside, with the company trading at the lower end of its price-to-earnings multiple relative to the ASX 200.

Held in: WAM Capital (ASX: WAM), WAM Research (ASX: WAX) and Wilson Asset Management Founders Fund

Thermo Fisher Scientific (NYSE: TMO)

Thermo Fisher Scientific, a leading provider of scientific research instruments and services, reported a strong Q3 FY2025 result last week. Reported revenues were up 5% year-on-year and adjusted earnings per share (EPS) were up 10%, ahead of consensus expectations. Bioproduction and Analytical Instruments showed particular strength. The company raised full year guidance for revenues, adjusted EPS and operating profit margin and reiterated its mid-term guidance of 3-6% organic growth and long-term guidance of 7%+ organic growth. It announced a strategic collaboration with OpenAI focused on embedding artificial intelligence (AI) into products and improving Thermo Fisher’s internal productivity. Management is optimistic on the tailwinds and potential for share gains from European biopharma companies establishing more US manufacturing facilities, as they seek to mitigate tariff risks. Thermo Fisher continues to demonstrate superior operational execution and innovation and is well placed to consolidate its market dominance as its end markets recover.

Held in: WAM Global (ASX: WGB)

Education Perfect (Intermediate Capital Group)

Education Perfect (EP) is a software company that provides educational resources such as learning materials and assessment tests to schools on a software-as-a-service (SaaS) basis. Its primary markets are schools in Australia and New Zealand, where it is among the largest platforms and the only digital product that offers a full school solution. EP is majority owned by KKR, a highly reputable asset manager with experience in the ANZ software space. WAM Alternative Assets has exposure to EP through a senior debt package provided by our investment partner Intermediate Capital Group, alongside other lenders. High switching costs, strong EBITDA margins and cash flow generation, and predictable revenue growth driven by prepayments for services, position EP as a reliable counterparty for WAM Alternative Assets’ private debt investment.

Held in: WAM Alternative Assets (ASX: WMA)

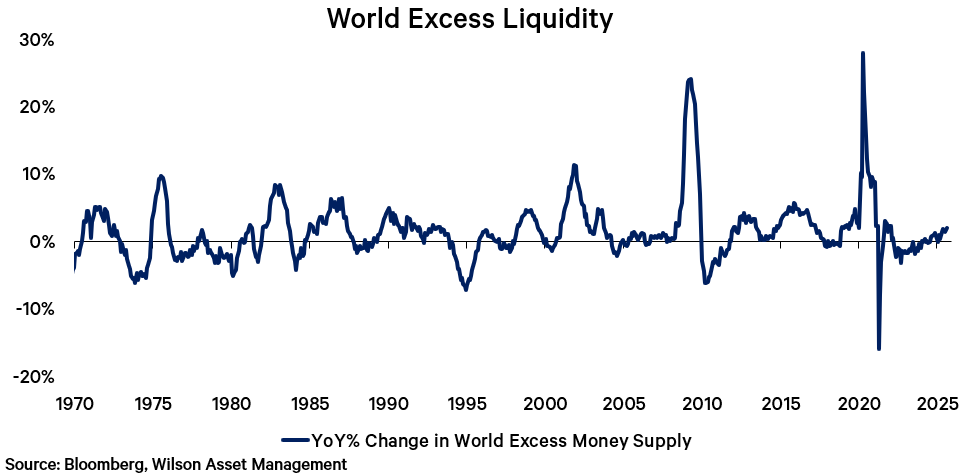

Too much money chasing too few goods

In the year to August 2025, world industrial production (IP) was up 2.7%, a below-trend rate of expansion that is historically consistent with lower commodity prices. While the release of more current data for September has been delayed by US government shutdown, it is interesting see that commodity prices have risen despite the uncertainty. One reason for rising commodity prices is growing scarcity – too much money chasing too few goods at the margin. We can see this in our measure of world excess liquidity growth, which measures the rate of expansion in broad money supply relative to the sum of activity growth and inflation. World excess liquidity has been gradually rising, foreshadowing better economic growth outcomes in the next year and supporting commodity prices.

WAM Income Maximiser Share Purchase Plan and investment portfolio update Q&A webinar

Register to join Lead Portfolio Manager Matthew Haupt and Portfolio Strategist Damien Boey for the WAM Income Maximiser Share Purchase Plan and investment portfolio update Q&A webinar on Wednesday 29 October 2025 at 11:00am (Sydney time).

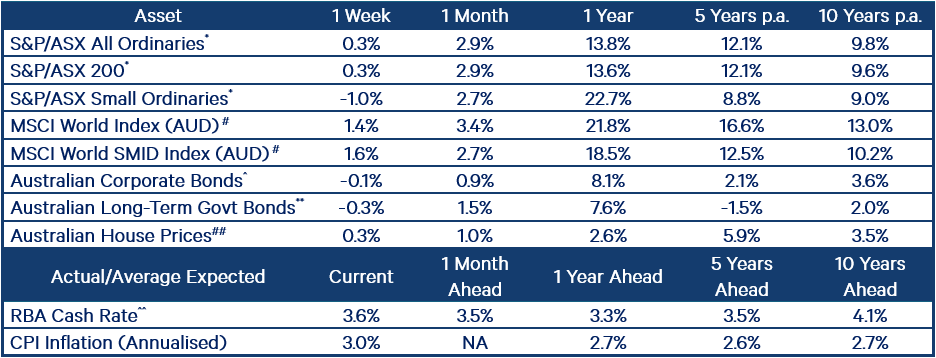

Index returns performance table